Last week I detailed why most economists – 58% according to one survey – think the U.S. economy will enter a recession in 2023. At the moment, I’m in the minority of economists (22%) who think a recession won’t begin until the second half of 2024 or later. Today, I’ll answer the question posed in the first part of this series: Why do some economists – a minority but not a tiny sliver of cranks – believe in the fabled “soft landing” scenario of inflation coming down and the economy staying (relatively) strong?

A Review of the Indicators

First, what do we mean by recession? I’m using the definition from the National Bureau of Economic Research (NBER), whose Business Cycle Dating Committee (a group of academic economists) is seen as the authority on dating the peaks and troughs of the economy. In NBER’s own words, a recession is “a significant decline in economic activity that is spread across the economy and that lasts more than a few months.”

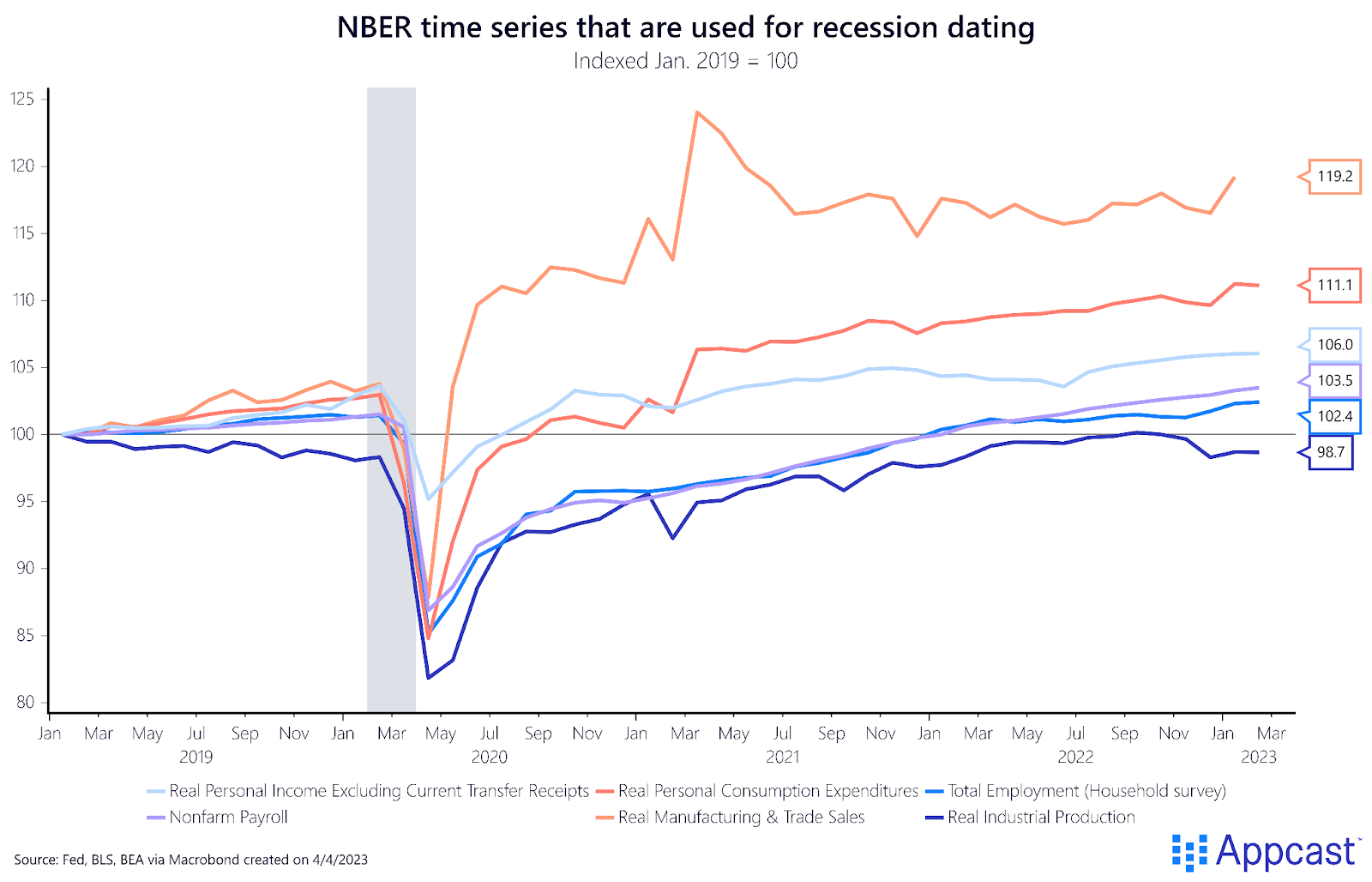

Over the past year, real GDP growth was a subdued 1%, which was below-trend but still positive. Admittedly, it did have two quarters of negative growth in Q1 and Q2 of last year, which is a “technical recession” used by some. However, the NBER doesn’t define a recession this way. Instead, it looks at a slew of indicators, not just one. Let’s review some of them. Real disposable income (after taxes and adjusting for inflation) is up. Consumer spending is up strongly. Manufacturing and retail sales are doing well. The one laggard – industrial production – is not off from its pre-COVID level by that much.

Most importantly, the labor market has been extremely strong. The two benchmark surveys used to estimate employment – nonfarm payrolls and the household survey – have been growing gangbusters.The unemployment rate is likely below NAIRU (non-accelerating inflation rate of unemployment), and earlier this year fell to 3.4% (the lowest since the Apollo moon landing in 1969). More useful as an indicator of full employment is the prime-age employment-to-population ratio, which has recovered to 80.5%, its level in February 2020. Overall, job growth has been on a tear, too, with net-new payroll employment up over four million in 2022. Nominal wage growth was the fastest in 40 years, even though it was outpaced by inflation for most workers.

Simply put: labor demand exceeds labor supply by about four million. Fed chair Jay Powell has said that reducing inflation back to target is likely going to require “some softening” in labor market conditions. We have a long way to go.

The current economy is not so bad. The labor market is quite strong. Consumers are spending strongly. It’s hard to claim that that’s a recessionary scenario – or even headed that way.

But what about rising interest rates? The thrust of the recession-is-coming argument is that tightening credit eventually takes its proverbial “pound of flesh” out of the economy. The key to the timing is how fast inflation gets back down to target. Jason Furman, the former top economist for President Obama, has convincingly argued that underlying inflation is too high, in the 4.5% range. He believes in a “wage-price persistence” – but wage growth may be reversing.

Right now, wage growth, according to various measures, has turned a corner but core prices have not (yet). My argument is that it’s simply a matter of time in a softening labor market.

The Case for No Recession in 2023

Thus we circle back to the NABE question I ended on in my first post, showing how little faith economists have in the Fed’s ability to get inflation under control. Why am I in the minority in having faith in the Fed?

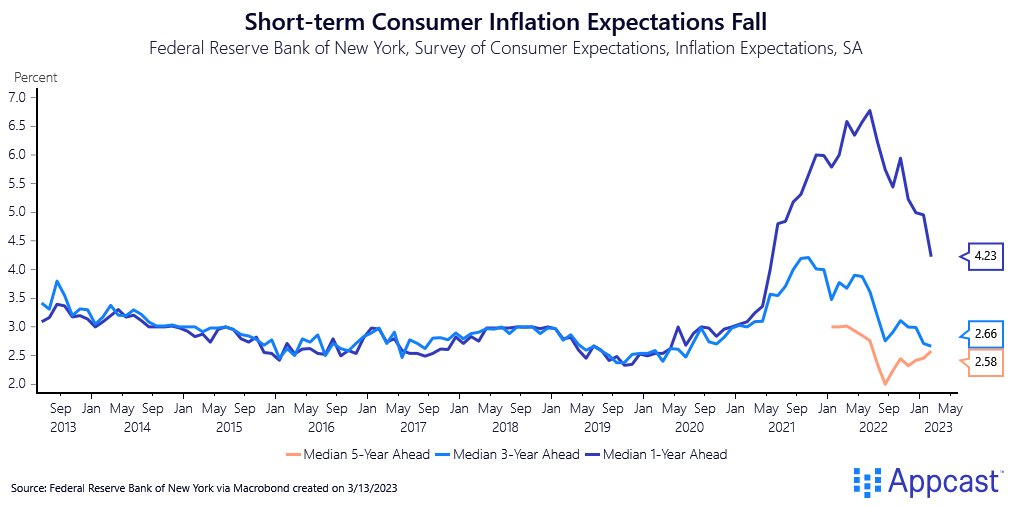

Well, because inflation expectations have remained well-anchored. See the consumer survey-based measures of expected inflation in the chart below, according to the New York Fed. With inflation expectations improving and the labor market already starting to soften, the Fed is on track to see core services inflation moderate in the coming months.

Thus inflation, in my view, will likely undershoot the Fed’s forecast in 2023, leading it to forestall further rate hikes (if not enact rate cuts). This, combined with the underlying momentum of the economy – especially the labor market – leads me to believe a “soft landing” is the most likely scenario. Those who believe the economy is doomed to suffer a recession in 2023 are ignoring that underlying strength – the NBER, you can be sure, will not.