This is part one of a two part series. For the full story, read Why Do Some Economists Believe A Recession Can Be Avoided?

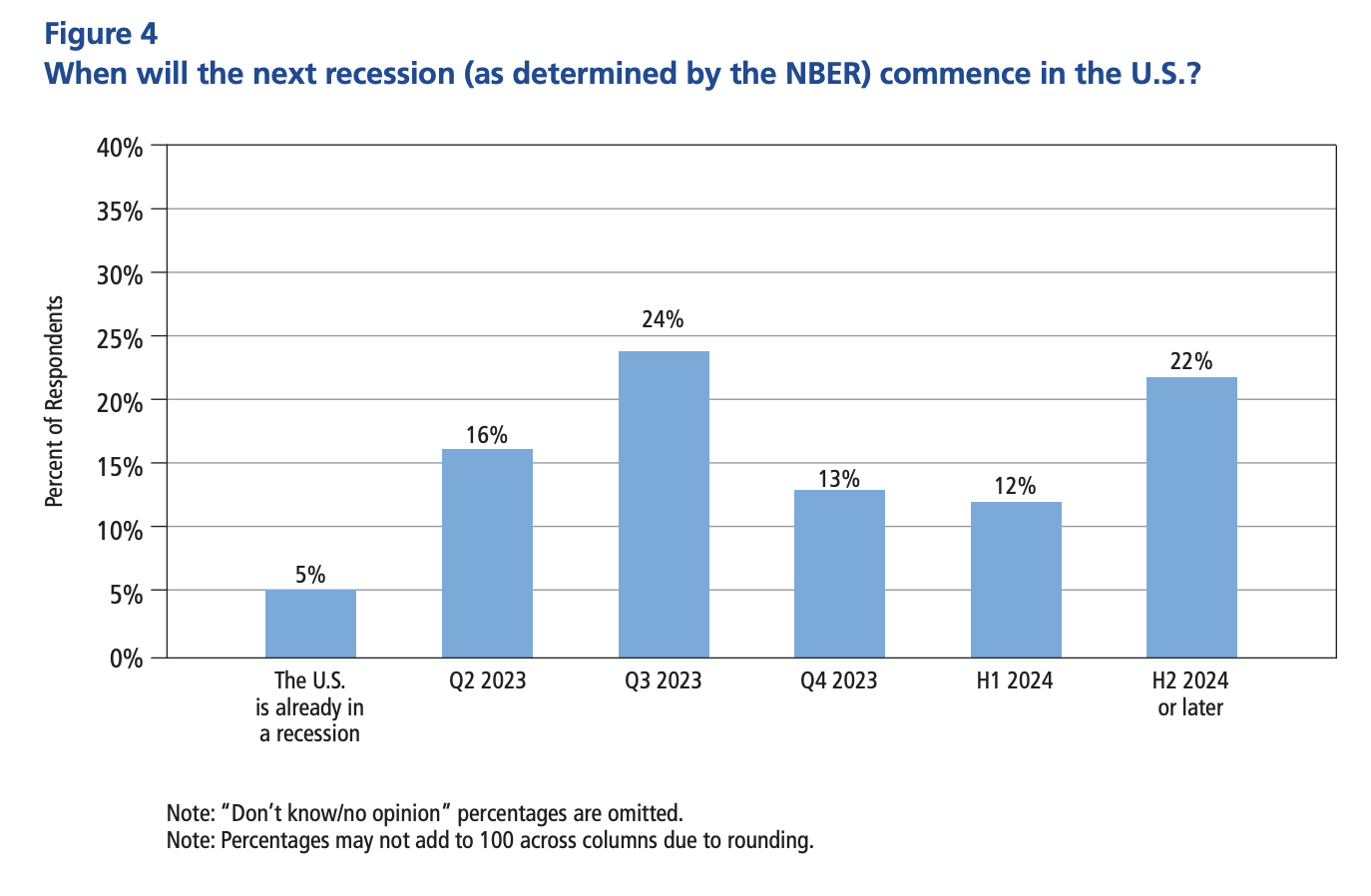

A majority of economists forecast a recession for the U.S. in 2023 – 58 percent, according to a survey from the National Association for Business Economics (NABE) released earlier this week on March 27. The chart below, from NABE’s release, shows that only 5% of surveyed economists think the U.S. is currently in a recession – and that share is down from 19% when last surveyed in August 2022. The most likely start of a recession is Q3 of this year, when 24% of NABE panelists expect a recession to begin.

The optimists, like myself, are a minority. 22 percent think a recession won’t begin until late 2024 or later. In a webinar I delivered on March 29, I have 60% odds of no recession in the U.S. this year. I’ll try to succinctly answer two questions:

- Why do most economists think a recession is likely this year?

- Why am I not one of them?

I’ll answer these questions in two articles. In the first, I’ll address the first question, and in the second I’ll explain why I’m in the minority. Before I do this brief exercise, I want to give the honest caveat: economic forecasting is a thankless, dispiriting task. If you submit forecasts regularly, you’re going to get it wrong sometimes. Especially in the post-COVID, land-war-in-Europe, bank-failure world of 2023, economic uncertainty is very high. But forecasts – good ones – don’t try to predict the future, and instead attempt to drive investments in the present.

Why Do Most Economists Think a Recession Is Likely This Year?

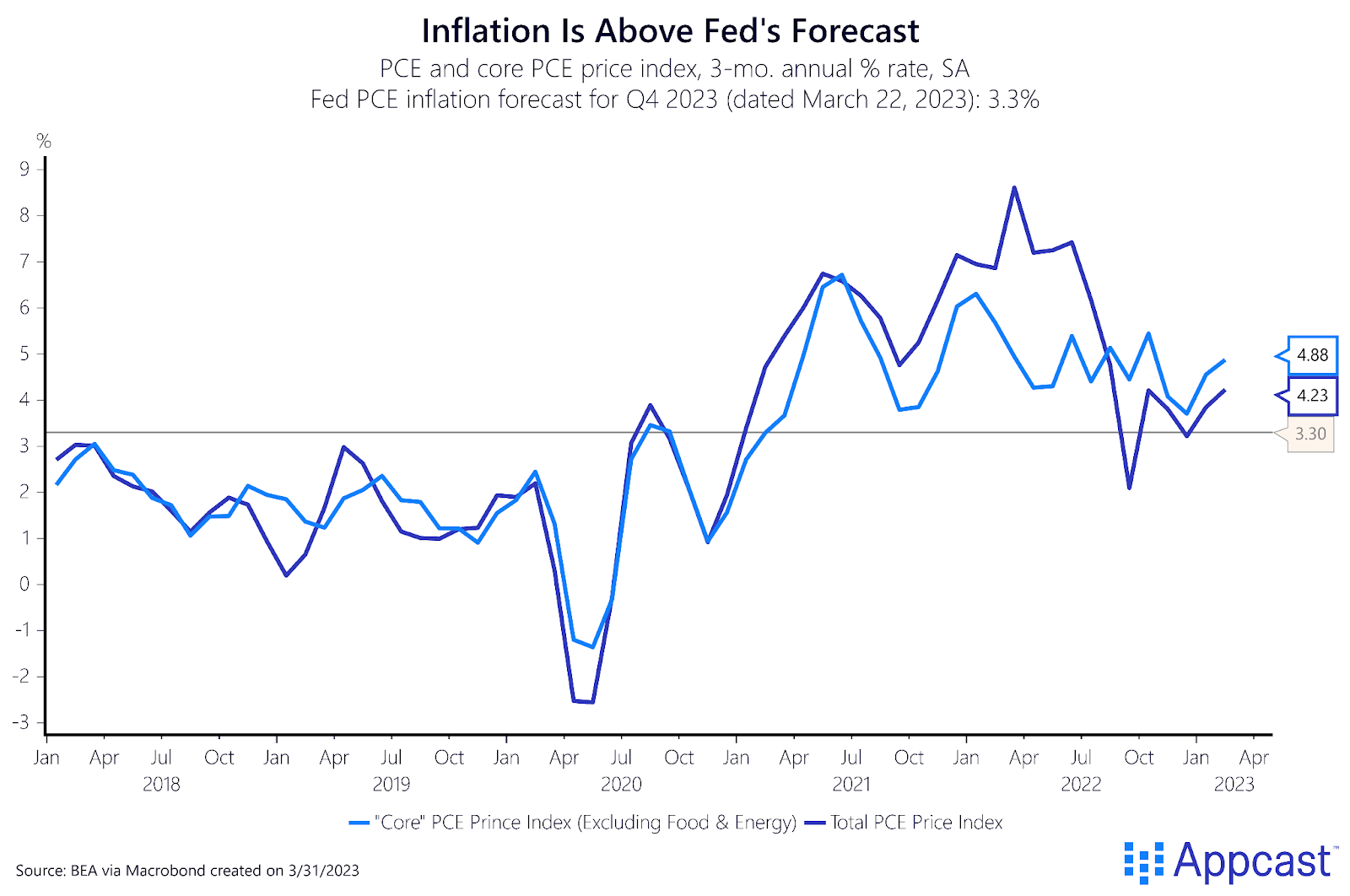

Inflation is the place to start. A recession is possible because inflation is too high and the Fed is consciously slowing the economy. First, on inflation, we learned this morning that the Fed’s preferred inflation index – the PCE price index – is growing above the Fed’s forecast for this year. Total PCE inflation grew at a 4.2% annual rate in the three months through February 2023. Core PCE inflation was up even more (4.9%). Both measures are above the Fed’s forecast of 3.3% price growth through Q4 2023 (an official forecast was released just last week).

Simply put, spending is rip-roaring strong. We see this in nominal GDP. That is current-dollar figures, not adjusted for inflation. The Mercatus Center, and David Beckworth in particular, produce an interesting estimation of what I consider nominal GDP’s capacity – what it’s expected to be (built off projections of national income from forecasters) relative to what it actually is.

Right now actual nominal GDP exceeds this expected “capacity” limit, reflecting an overheating economy. To be clear, this is a damning chart for those (myself included) who thought inflation has been primarily supply-driven. That may have been true earlier in the expansion but it’s likely less of a factor now compared to this strong, demand-driven inflationary impulse.

Hence, the rapid interest rate hikes –the Fed wants to cool this economy off. The slowing was evident this week in the third and final reading on Q4 2022 real GDP growth. The second half of 2022 saw 2.9% growth, whereas earlier last year real GDP fell by 1.1%. We won’t get the initial estimate of real GDP growth until late April, but the Atlanta Fed’s excellent GDPNow model estimated 3.2% growth in Q1 2023. (Yes, I’m biased, as I used to work there).

While these growth numbers aren’t terrible, they could possibly be deceiving. Underlying real GDP growth can perhaps be better understood by removing the often-volatile categories of government, trade, and inventory fluctuations. This is called “real final sales to private domestic purchasers” and if you say it out loud, you’re an instant hit at your neighbor’s barbecue. It is slowing. Growth in the second half of 2022 was positive, but barely so(+0.5%).

It seems the Fed’s “cool it” campaign is working, at least according to lagged GDP data. However, today we got another report, and it showed that inflation-adjusted, after-tax income – also known as disposable personal income – has risen a modest 3% over the last three years. And it’s still trending up.

That income is fueling spending, which is powering a strong labor market, and that feeds through to healthier family checking accounts, which powers more spending… You see how the momentum of an overheated economy is a challenging obstacle to get inflation back to normal.

This morning’s data on February personal spending showed consumers had a surprising splurge on things (goods) as opposed to services. Inflation-adjusted consumer spending on goods in the three months through February has been very strong, led by an enormous (perhaps anomalous) boom in durable goods in January.

Economists Think The Fed Has A Long Battle

In conclusion, according to most economists (but not me!) a recession is likely in 2023 because the Fed just simply isn’t going to slow the run-away train of an overheating economy. In this view, inflation remains stubbornly entrenched, and the pain from tightening credit takes longer to eventually get its pound of flesh in the form of a slowdown. The lack of faith in the Fed’s inflation-fighting capability is seen in this question from the aforementioned NABE survey: nearly 70% think the Fed has a long-term battle against inflation (it won’t fall to 2% by the end of 2024).

Tune in early next week for part two, where I’ll detail why I think the consensus view is too pessimistic. And I’ll defend why I give only a 40% chance of a recession in 2023.