Inflation was red hot in May. The consumer price index (CPI) rose by 1% in that month alone, and was up 8.6% year-over-year. These numbers dashed hopes (including mine) of a cool down in prices, perhaps with inflation peaking in March. Unfortunately, that’s not happening. A key macroeconomic question remains: Is high nominal wage growth driving inflation higher?

Until recently, the answer has been pretty clearly ‘no.’ The recent price acceleration can be largely attributed to goods prices. During the pandemic, as consumers shifted their consumption away from services (haircuts, restaurant meals, etc.) to goods (vehicles, furniture, etc.), and supply chains came under stress. Backlogs ensued, and goods – things – became more scarce. Consequently, prices for those goods rose.

In recent months, as the global economy’s supply chain problems have begun to lessen, the primary culprit behind higher inflation became rising energy costs, paired with increasing food prices. In May, this trend continued; energy (34.6% year over year) and food energy prices did indeed drive price growth (particularly gasoline, which was up 49% from a year prior).

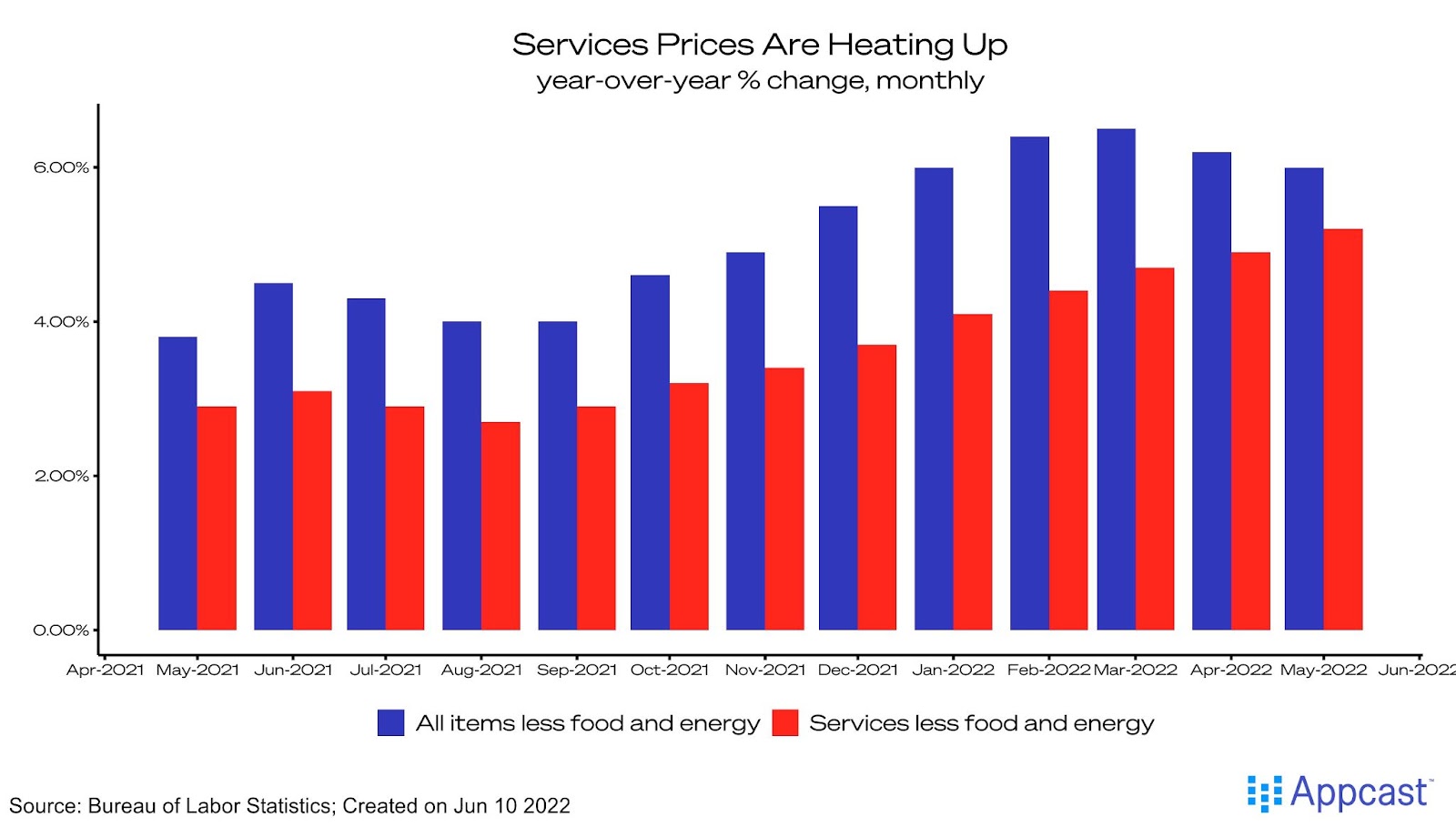

However, a concerning data development has caught our attention: it seems that services prices are heating up just as goods prices are cooling (see chart). “Core” services prices – stripping out volatile food and energy service components – have steadily risen. Given that services-based businesses typically have a higher labor cost share, and that nominal wages have been rising briskly, this could push inflation dynamics toward a dreaded wage-price spiral.

This trend might just be a reflection of the post-COVID economy opening up. Services-based companies may be trying to pass on the higher labor costs they’ve incurred over the last 15 months to their staff. If a wage-price spiral does take hold, the Federal Reserve’s task of combating inflation will get significantly harder. Again, nominal wages do NOT appear to be the main driver of inflation in recent months, but I worry that could change. Having misjudged the previous month’s CPI report, I’m more skeptical now of the claim that inflation will subside as goods prices deflate. Going forward, the potential for nominal wage growth to drive inflation higher is a major risk to the economy.