On Wednesday, the Federal Reserve left interest rates unchanged after 10 consecutive hikes since March 2022. The Fed revised up its expectation for growth in 2023 and revised down how much it expects the unemployment rate to rise. In other words, the Fed acknowledged a recession is unlikely this year.

“The labor market has surprised many, if not all, analysts over the last couple of years with its extraordinary resilience,” said Chair Jay Powell, before noting that supply and demand in the labor market are coming into better balance. We see that the labor market remains tight but is becoming marginally less so as the year progresses, as shown in the chart below.

However, this was something of a “hawkish pause” in that the Fed signaled openness to interest rates moving higher later this year. There is disagreement within the committee over how much (if at all) rates need to go up further. The key variable will, of course, be inflation. The latest May Consumer Price Index (CPI) report released this week showed core inflation elevated at around 5%, as shown in the chart below. The light blue line (core CPI, stripped of volatile food and energy prices) is roughly flat over recent months. This stickiness prompted the Fed to revise up its forecast for core inflation later this year. Side note: the Fed’s inflation target is based on the Personal Consumption Expenditures (PCE) price index, which tends to be lower than the CPI.

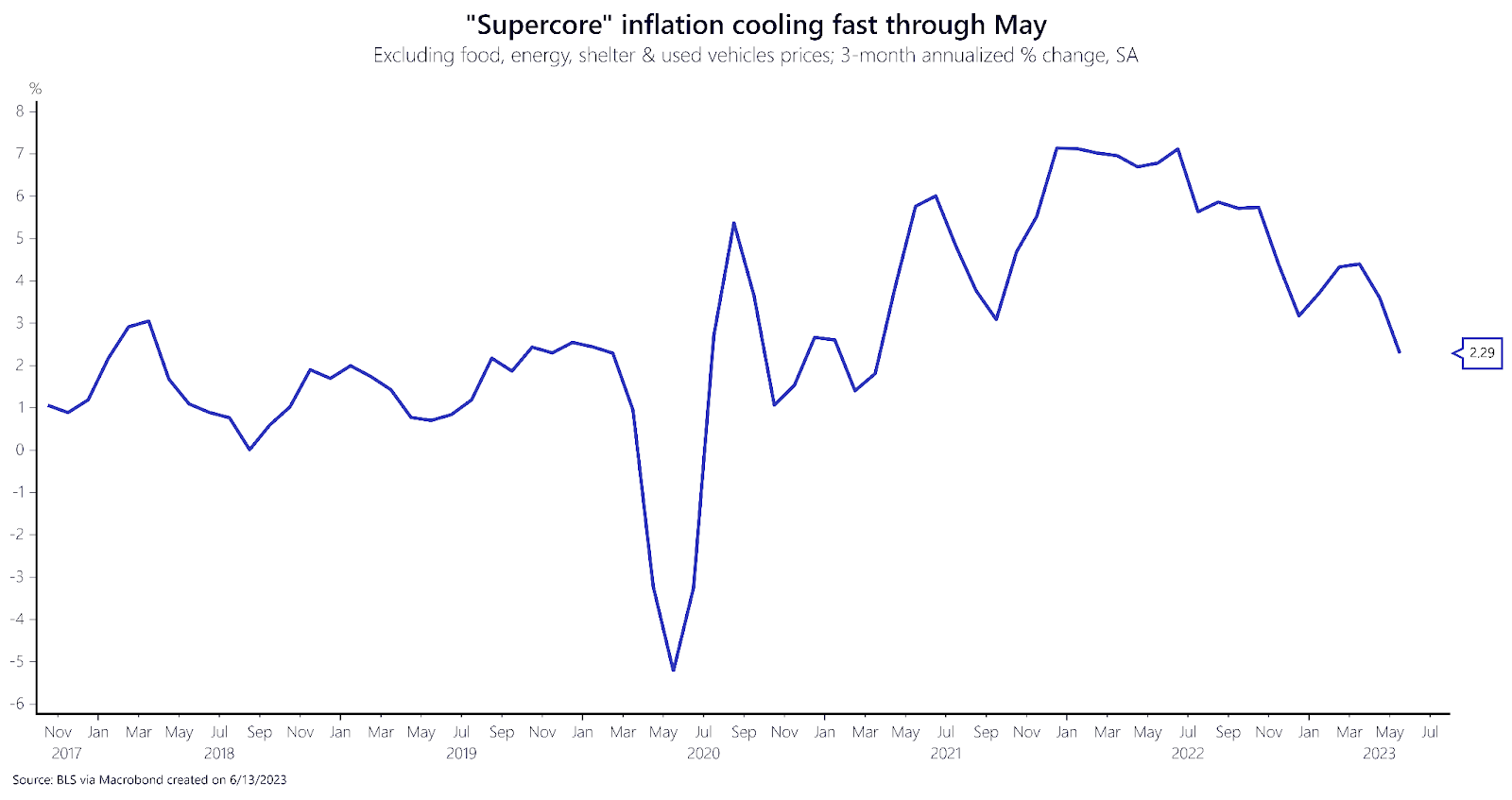

But there was some good news in the CPI report: underlying inflation is likely cooling. “Supercore” inflation readings exclude not only volatile food and energy prices, but also shelter and vehicle prices that move with long lags. In the three months through May, “supercore” inflation was growing at a 2.3% annual rate. In May 2022, this was at 6.8%.

This is an encouraging sign that underlying price pressures are rolling over and trending toward the Fed’s 2% inflation target. However, we’re not there yet – far from it. And while the Fed refrained from raising interest rates today, it’s not clear they’re going to pause in late July – Powell commented that it will be a “live” meeting, meaning a rate hike is a possibility. The truth is that the Fed is highly uncertain about the future of core price growth. The chart below shows FOMC members’ assessment of uncertainty over core PCE inflation, compared to the past 20 years of historical data. They can respond in one of three ways: the current uncertainty over inflation is “lower”, “broadly similar”, or “higher” than over the past two decades. Almost all members continue to report inflation uncertainty as “higher.”

What does this mean for recruiting?

It’s heartening that the Fed has revised up its 2023 forecast for growth, especially while it expects the unemployment rate to end the year lower than it previously forecasted. So all-in-all, the Fed acknowledges that the U.S. economy isn’t in a recession at the moment, in part because of the labor market’s “extraordinary resilience,” as Powell said, with labor demand far exceeding supply. But the key variable remains inflation – the tentative signs we’ve gotten so far that inflation may be turning the corner aren’t enough to convince the Fed to pause for good. If future inflation readings moderate, the Fed will have sufficient evidence to pause this rate hiking cycle permanently later this year – a welcome reprieve for recruiters and workers alike.