Recessions are a painful, yet natural, part of economic reality. A recession is notoriously hard to define, but the most closely followed definition comes from the Business Cycle Dating Committee of the National Bureau of Economic Research (NBER).

The NBER committee defines a recession as “involving a significant decline in economic activity that is spread across the economy and lasts more than a few months.” Needless to say, that is pretty vague. Sometimes, the NBER doesn’t even follow its own rule; the recession that occurred in 2020 lasted only two months, but was considered deep enough that it was classified as such.

The NBER follows a wide variety of economic indicators. Understanding where these indicators fall gives economic forecasters a head start in recognizing if a recession is upon us.

Unemployment Rate

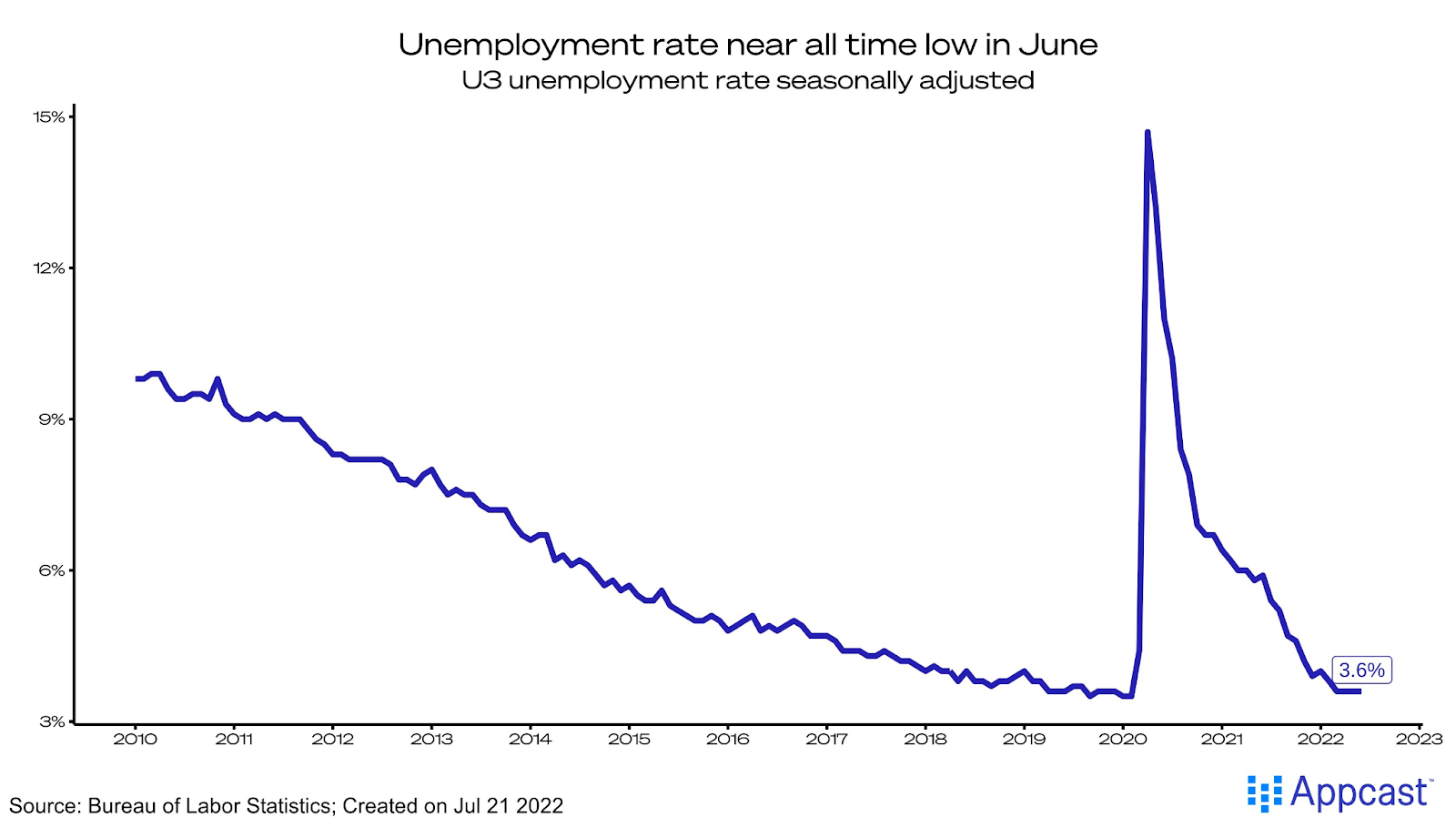

A high unemployment rate is a telltale sign of a sick labor market and the most painful feature of a recession. During the last two recessions starting in 2007 and 2020, the unemployment rate rose to highs of 10.0% and 14.7%, respectively.

In June 2022, the unemployment rate was historically low, at 3.6%. The current labor market is fundamentally strong, something not normally observed when the economy is approaching – especially, already in – a recession.

Sahm Rule

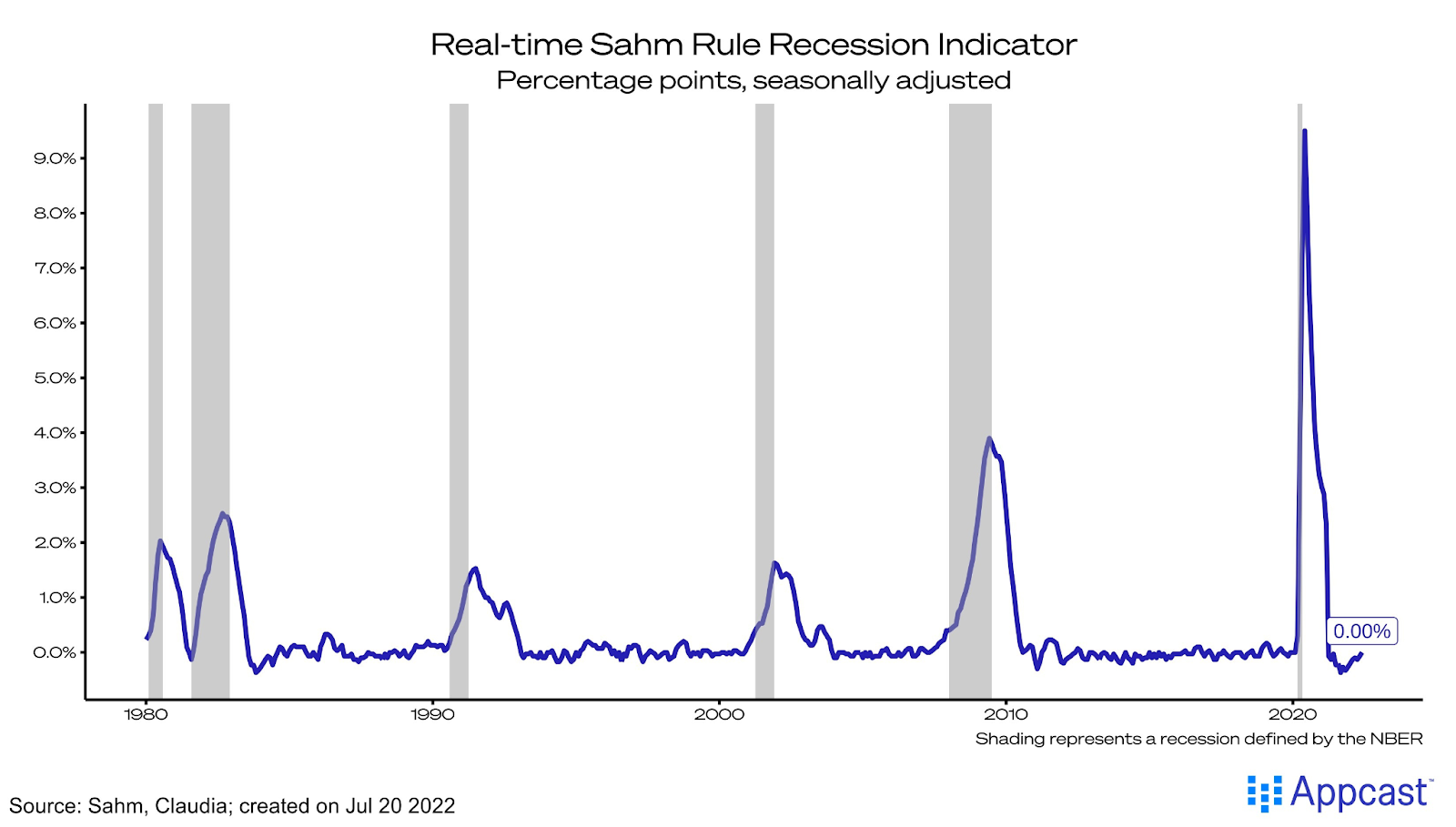

The Sahm rule is a relatively new recession indicator. Engineered by Claudia Sahm, a former economist at the Federal Reserve, this rule states that when the three-month moving average of the unemployment rate rises half a percentage point relative to its low of the previous year, the economy has or is very likely to enter into a recession.

This rule is designed to recognize a recession immediately – a much more timely indicator than the NBER’s classification, which can take over a year to be released.

Currently, the Sahm rule stands at 0.0% – no sign of a recession. Sharp-eyed forecasters will be watching its fluctuations closely, waiting for the rule to rise by 0.5 percentage points.

Yield Curve

The stock market is not the economy, but investors are watching the “real” economy closely. Their decisions are (usually) backed by sound economic advice. For that reason, a negative yield curve spread has been a trusted indicator of recession for economic forecasters for decades.

A negative yield curve spread occurs when the yield (or interest rate) of the 3-month treasury bond is greater than that of the 10-year treasury bond. Another yield curve generally regarded as a popular recession indicator is that of the 2-year and 10-year treasury bonds. Usually, a negative spread precedes a recession by 1-2 years. A negative yield curve signals that investors expect future interest rates will be lower than today – that is, the economy will weaken in the future to such an extent that the Fed will need to cut rates to revive activity.

The most recent negative yield spread occurred in February 2020, amid the COVID-19 recession.

Industrial Production

The level of industrial production shows the output of several US sectors; it is a solid indicator of the strength of the productive capacity of the economy. It measures the output of manufacturing, mining, construction, and more.

In June 2022, industrial production was up 4.16% from a year ago, implying the strength of our economy is still relatively stable.

Gross Domestic Product

A popular definition of a recession, though one not followed by the NBER, is two consecutive quarters of declining real GDP. Many past recessions have featured declining GDP, and it is a telling indicator of a slowing economy.

In Q1 of 2022, real GDP growth was -0.4%. The Q2 GDP data will be released next week, and if another quarter of decline is reported, many will be quick to declare the US economy is in a recession. Without considering the other indicators listed above – and several more – the picture is incomplete.

Conclusion

For brevity’s sake, not every important recession indicator is included above. Other fluctuations that forecasters watch are those of consumer spending, the real estate market, durable goods spending, and more.

Recessions are hard to predict; even professionals can get the art of forecasting wrong. Causes of a recession are varied and often difficult to protect against. In this case, high inflation may cause the Federal Reserve to slow the economy to a halt, inducing a recession. The NBER and forecasters will be watching these indicators and more closely in the weeks and months to come.