The U.S. labor market continues to hum along. In October, 261,000 net new jobs were created – above market expectations for approximately 200,000 – but the unemployment rate increased to 3.7% from 3.5% (which was a 50-year low). Labor force participation slumped, which is bad news – particularly for hiring organizations. But wage growth continues to moderate, which is good news from the perspective of the Fed’s goal of taming inflation.

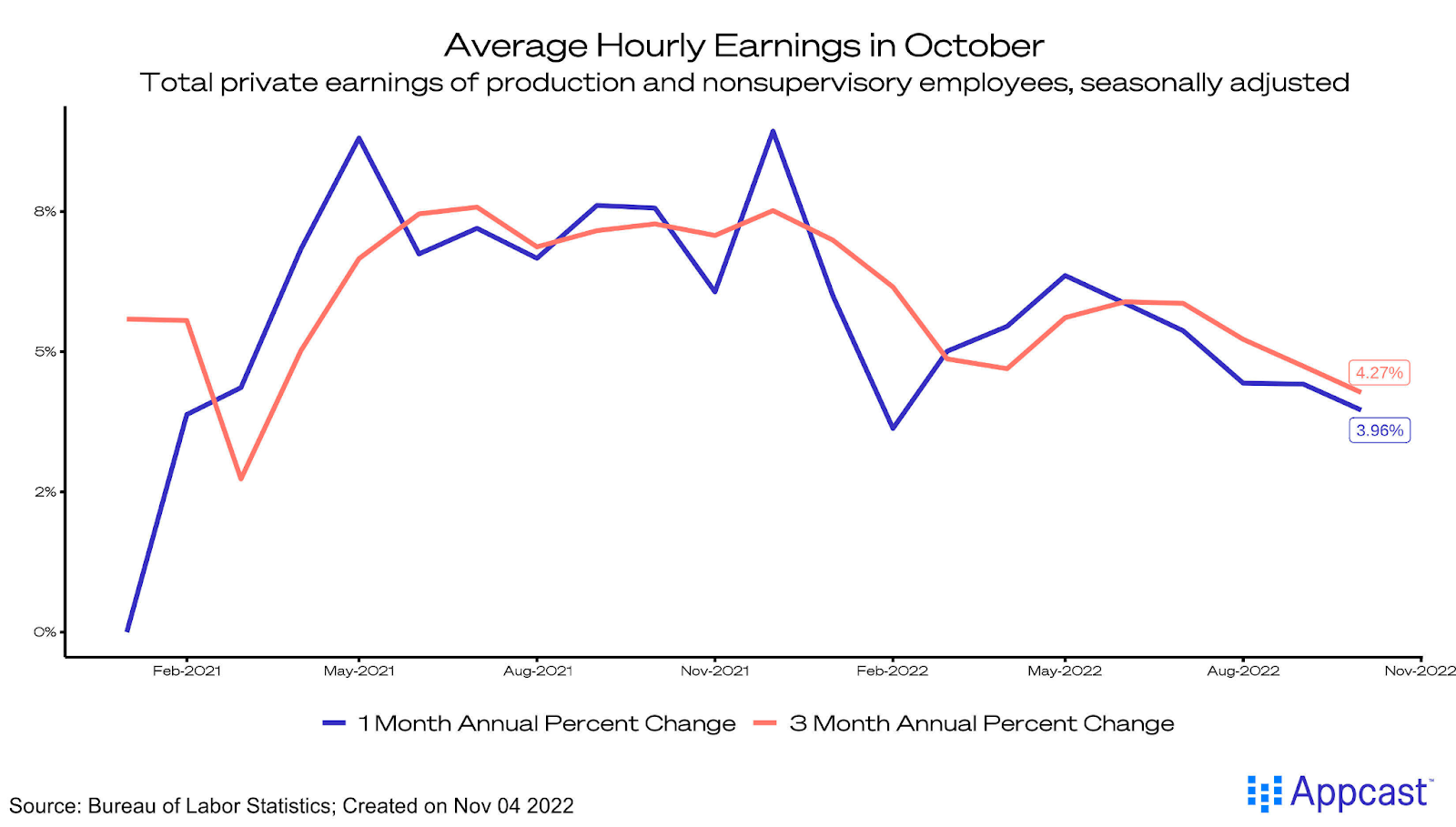

Good news: Wage growth moderating

A “good” sign in this report is that wage growth continues to moderate. We put scare quotes around “good” because policymakers are keen now to avoid above-trend wage growth pouring gasoline on the inflationary fire. Average hourly earnings (3-month annualized rates, for private sector non-managers) grew at 4.3%. The 1-month rate was below 4%. Clearly wage growth is cooling, as the Fed would hope to see from its aggressive interest rate hikes.

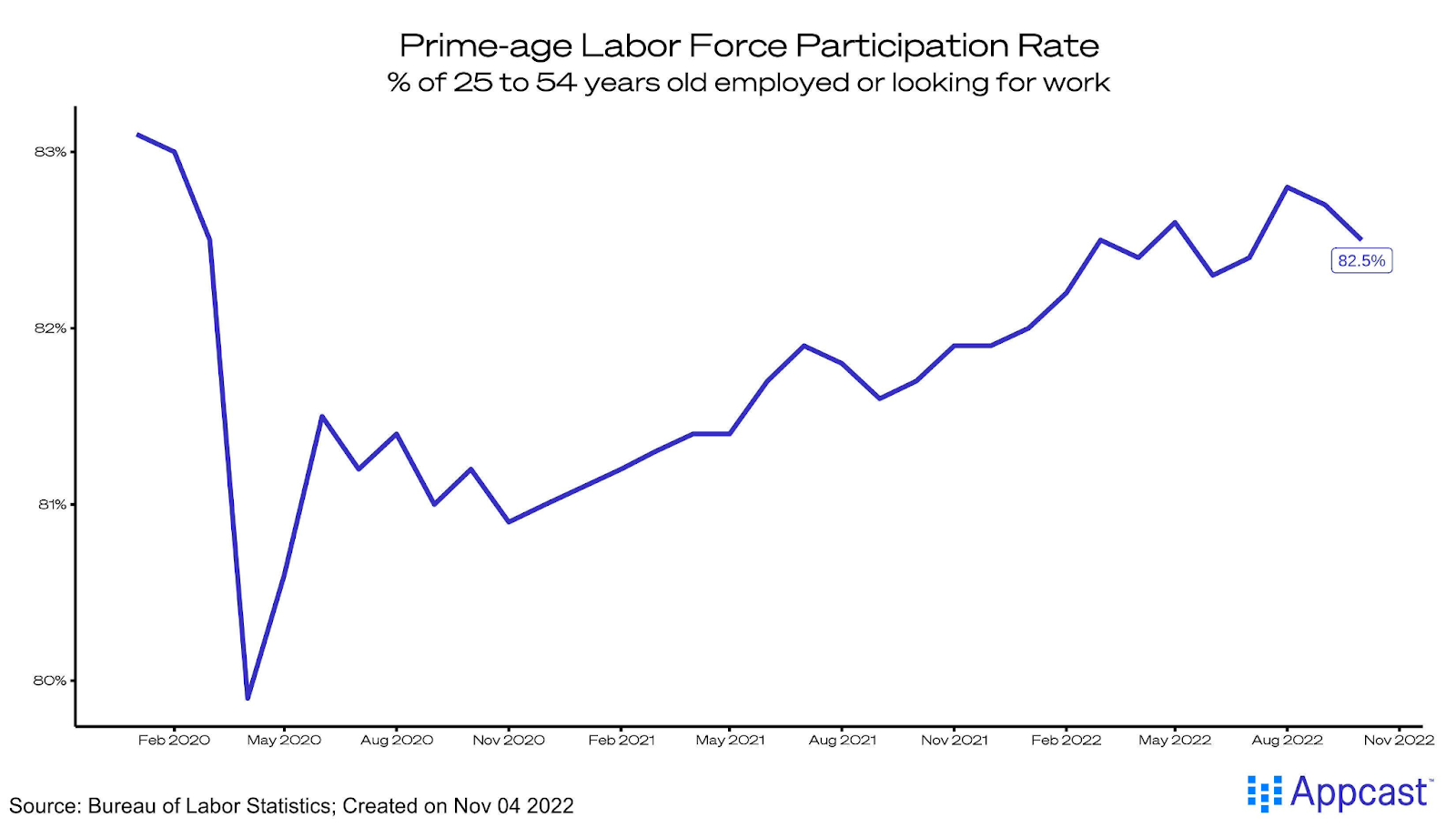

Bad news: Labor supply stalling

The household survey – which is used to calculate the unemployment rate and measures of labor supply – can be volatile. But over the last two reports, from August to October, measures of labor force participation have gone in reverse. The prime-age labor force participation rate declined to 82.5% in October, from 82.8% in August. Similarly, the prime-age employment-to-population ratio moved to 79.8% from 80.3%.

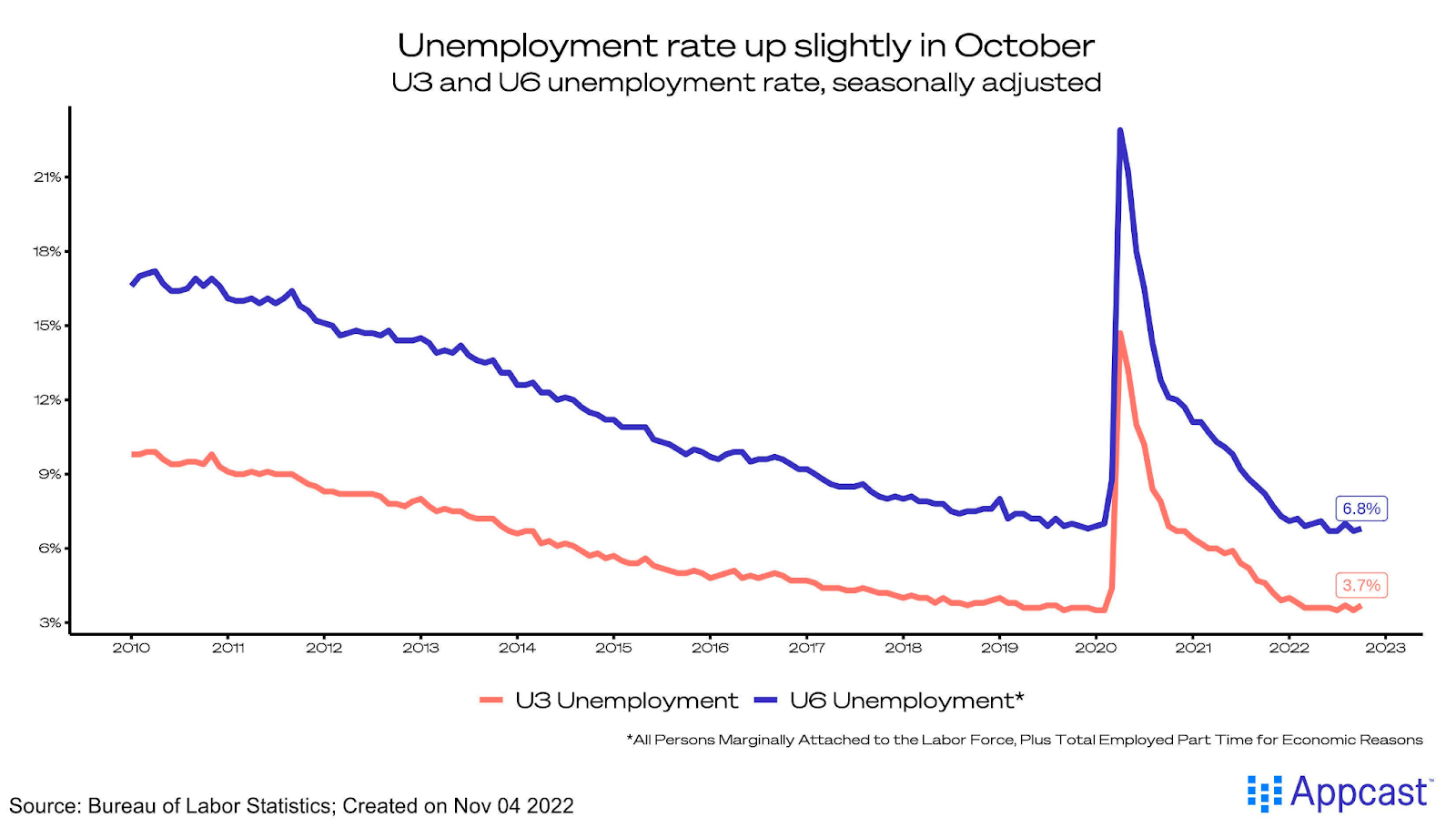

The benchmark unemployment rate (U3) rose from 3.5% to 3.7%, back to where it was in August. The same increase occurred in a more comprehensive measure of unemployment (U6), which includes discouraged workers and those working part-time for economic reasons.

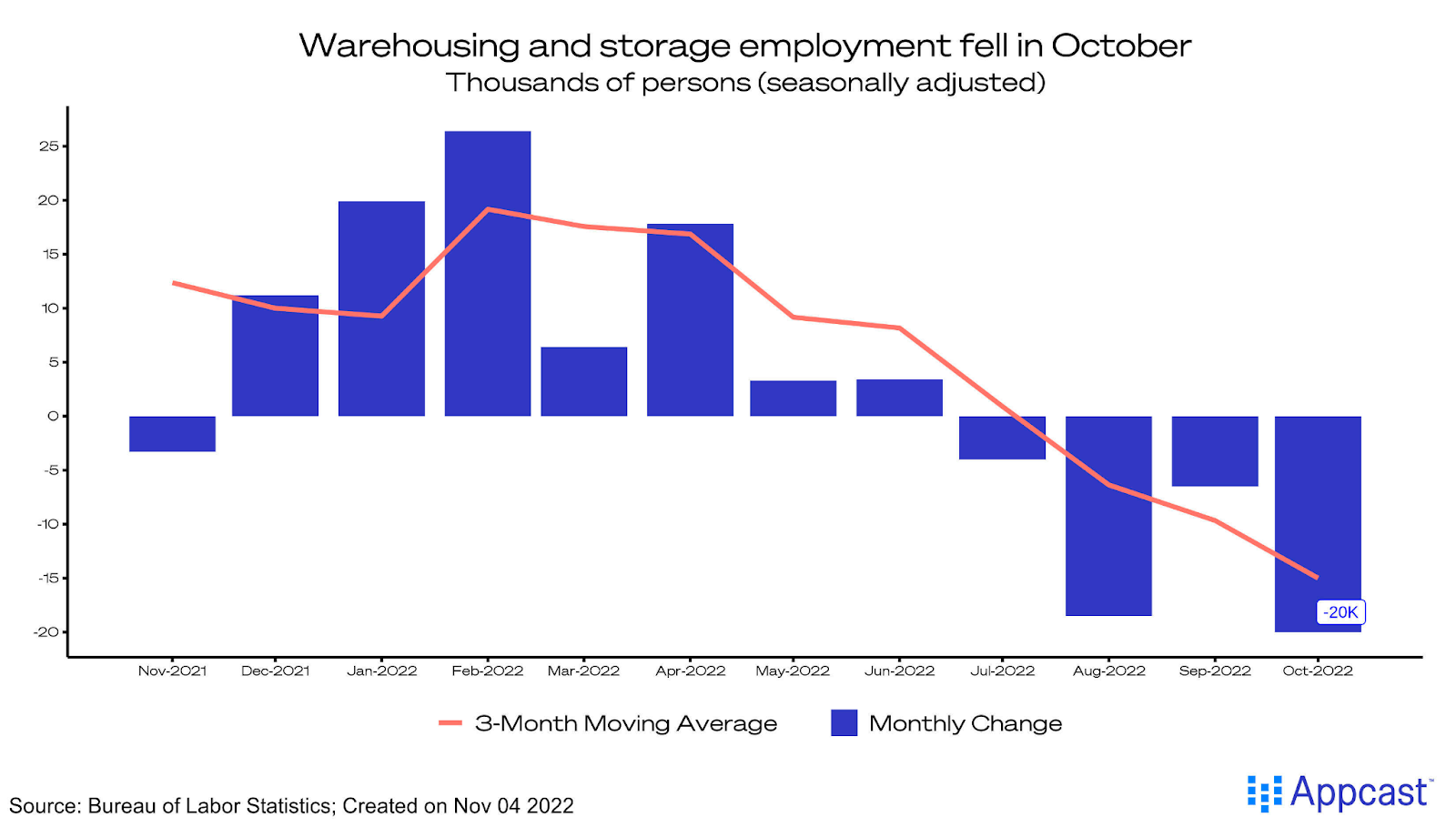

Neutral news: Powerhouse industry shifts

Warehousing jobs have been a powerhouse for the U.S. economy in the recovery since 2020. But after flailing this summer, warehousing is now cutting – with 20,000 jobs lost in October. Shifting consumer demand from goods to services has hit this sector particularly hard.

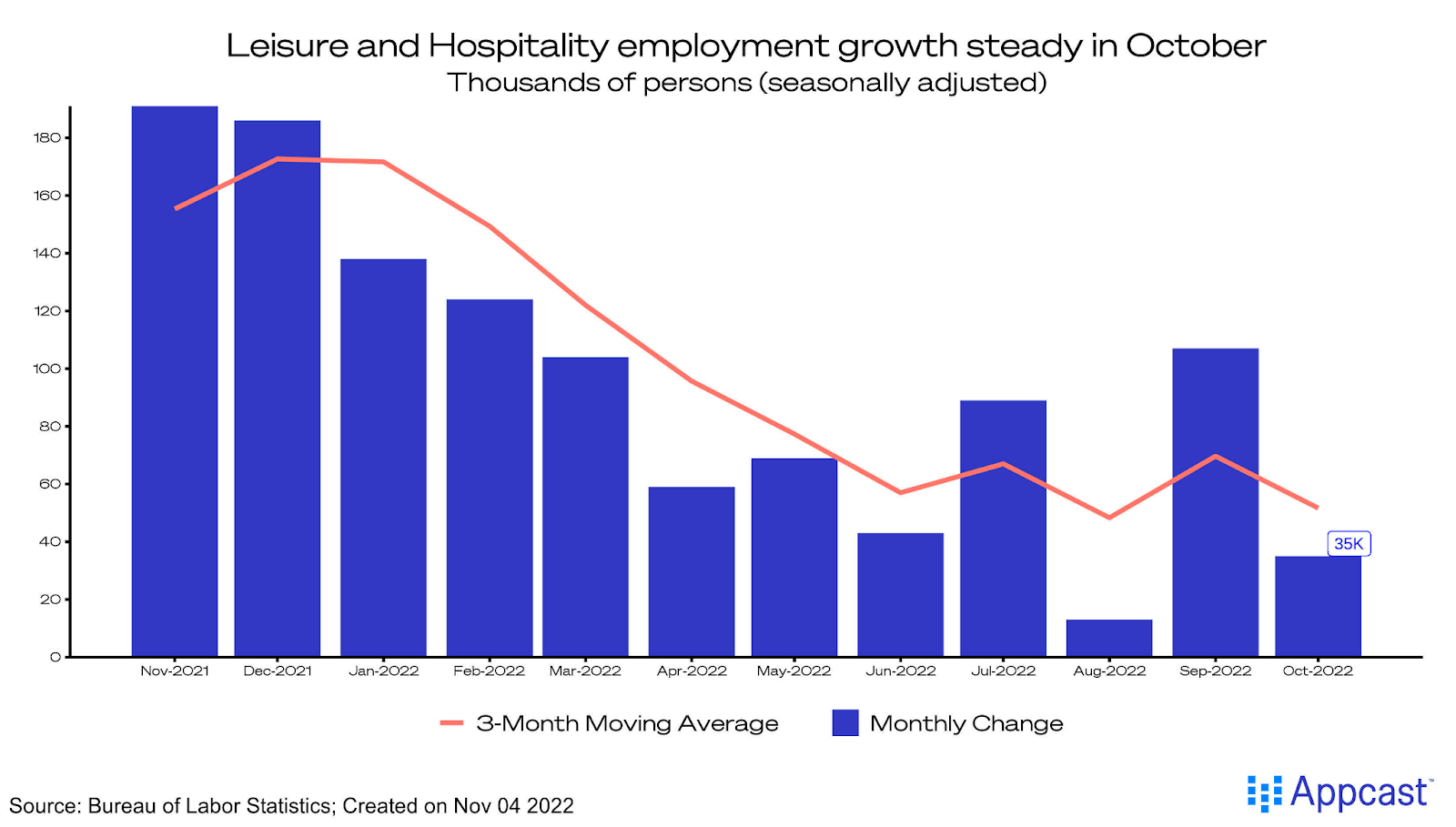

Leisure and hospitality jobs have been booming recently but cooled a bit last month (up just 35,000). Recently, gains have been choppy in the industry – the robust recovery the sector experienced earlier in the year is transforming into steady gains.

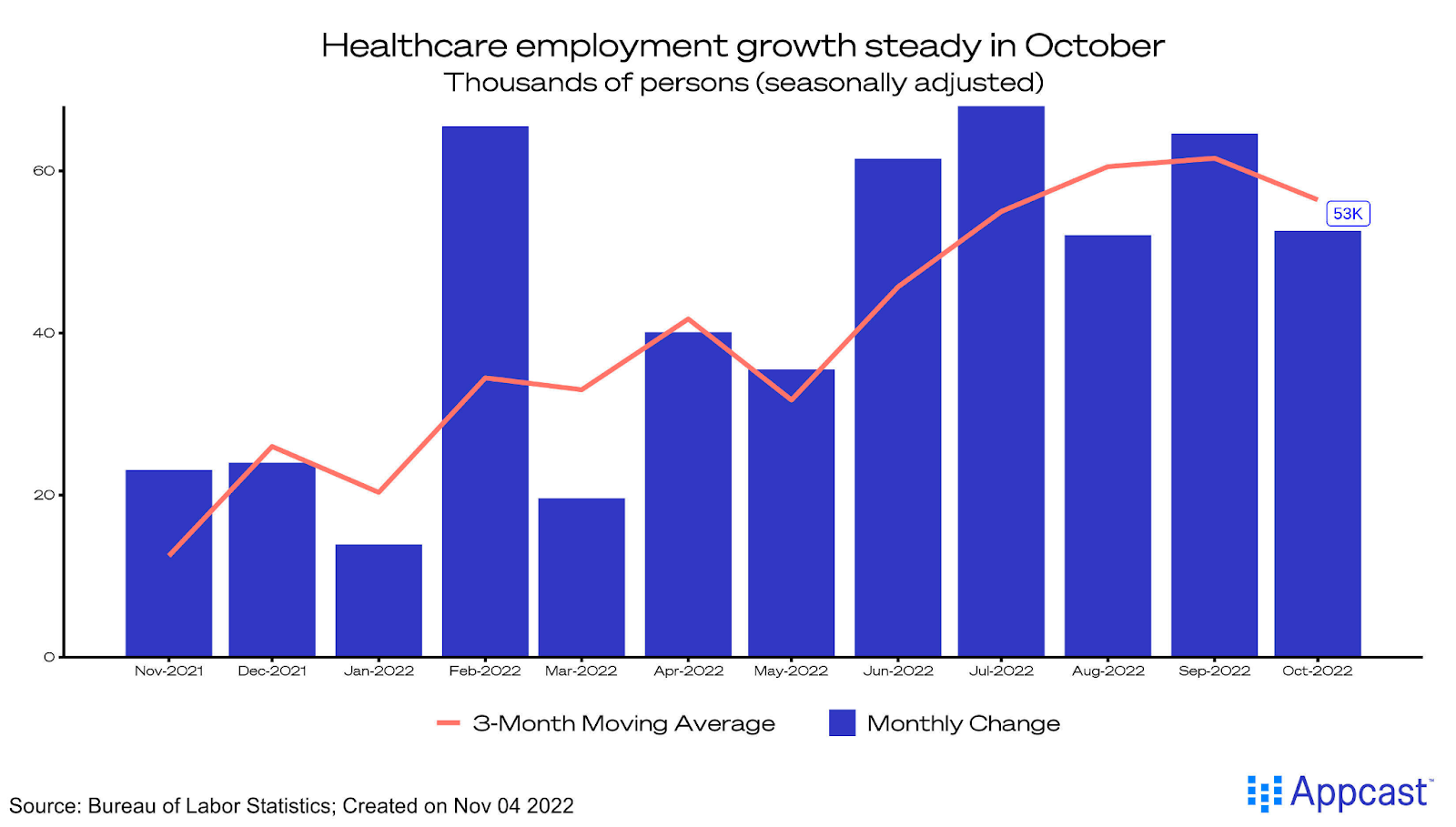

Healthcare, however, is picking up its hiring (+53,000). The sector is finally emerging from the shadow of the pandemic. As fears of COVID-19 subside, so too does the recent stigma surrounding healthcare professions. The sector has had a difficult period of recovery – but the latest trends point to an emerging powerhouse sector.

What does this mean for recruiters?

The labor market continues to be a patch of blue sky in an otherwise stormy economy. Job growth is strong despite recession fears, and wage growth is moderating (but still high). The issue for the economy – and for recruiters specifically – is the declining labor force participation rate. If workers continue to sit on the sidelines of this hot market, labor market imbalance will persist. With demand so high, competition will remain tight in the world of recruitment.