Inflation has seeped into our economy and taken over public discourse. And, though we are all obsessed with inflation and where it lies, it continues to confuse and infuriate us. Looking at price increases one way can show cooling, another way spells something more troubling. In short, it’s complicated.

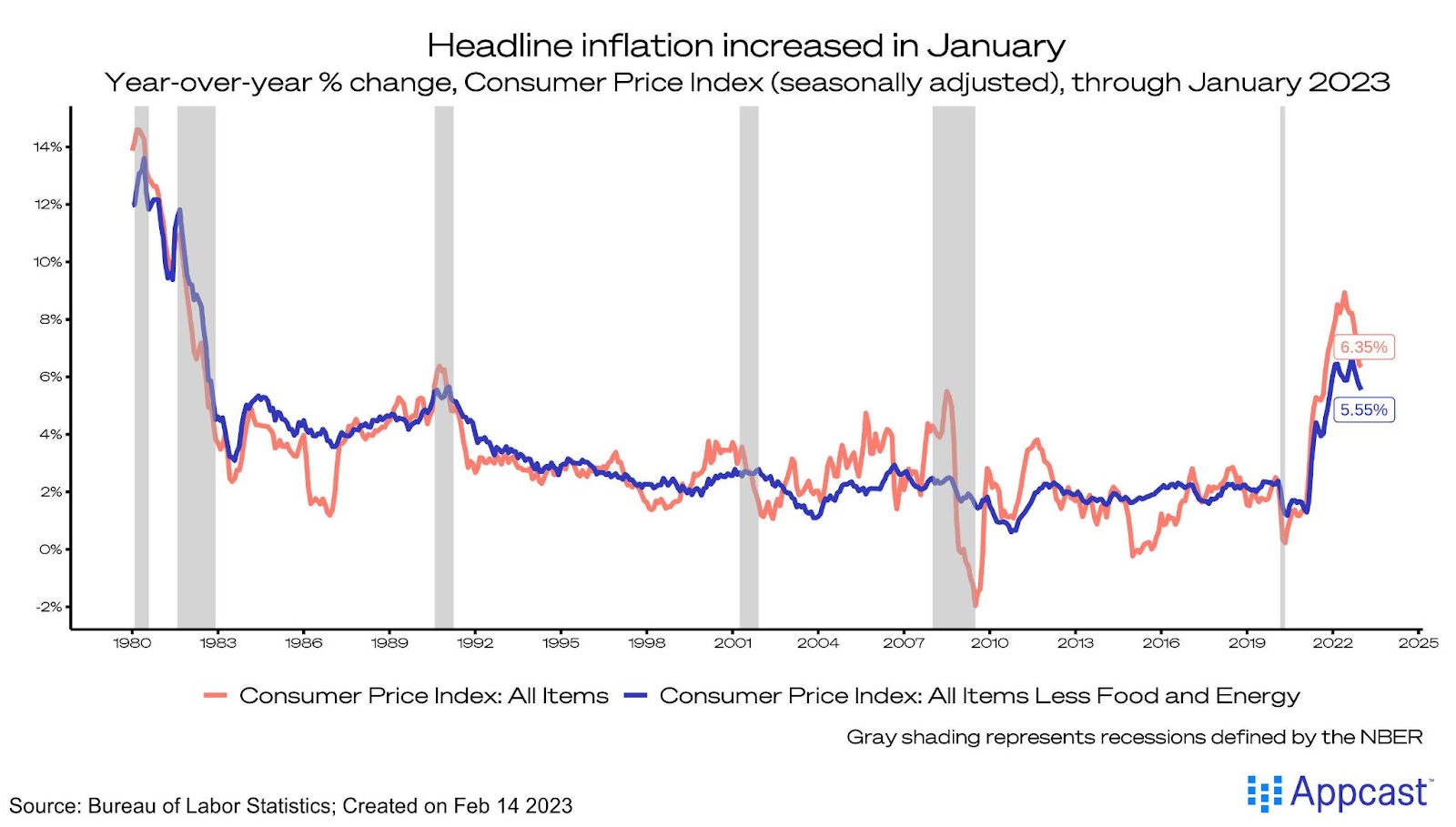

On Tuesday, January’s Consumer Price Index report showed that prices were up 6.35% from the year before, the smallest year-over-year increase since 2021. Core inflation, stripped of volatile food and energy prices, increased just 5.6% from the year before. So everything’s good, right? Not necessarily. Inflation is not a single number!

Month-over-month, prices increased 0.5%, and the disinflation of 0.1% in December was revised up – turns out there was no disinflation in 2022 after all. The short-run inflationary pain may be greater than we initially believed.

To be sure, these increases are impacted by a price pressure that some have dismissed as misleading: the housing index, which rose 0.7% month-over-month and contributed to the strong monthly increase. The official housing index is famously lagged and does not account for new leases.

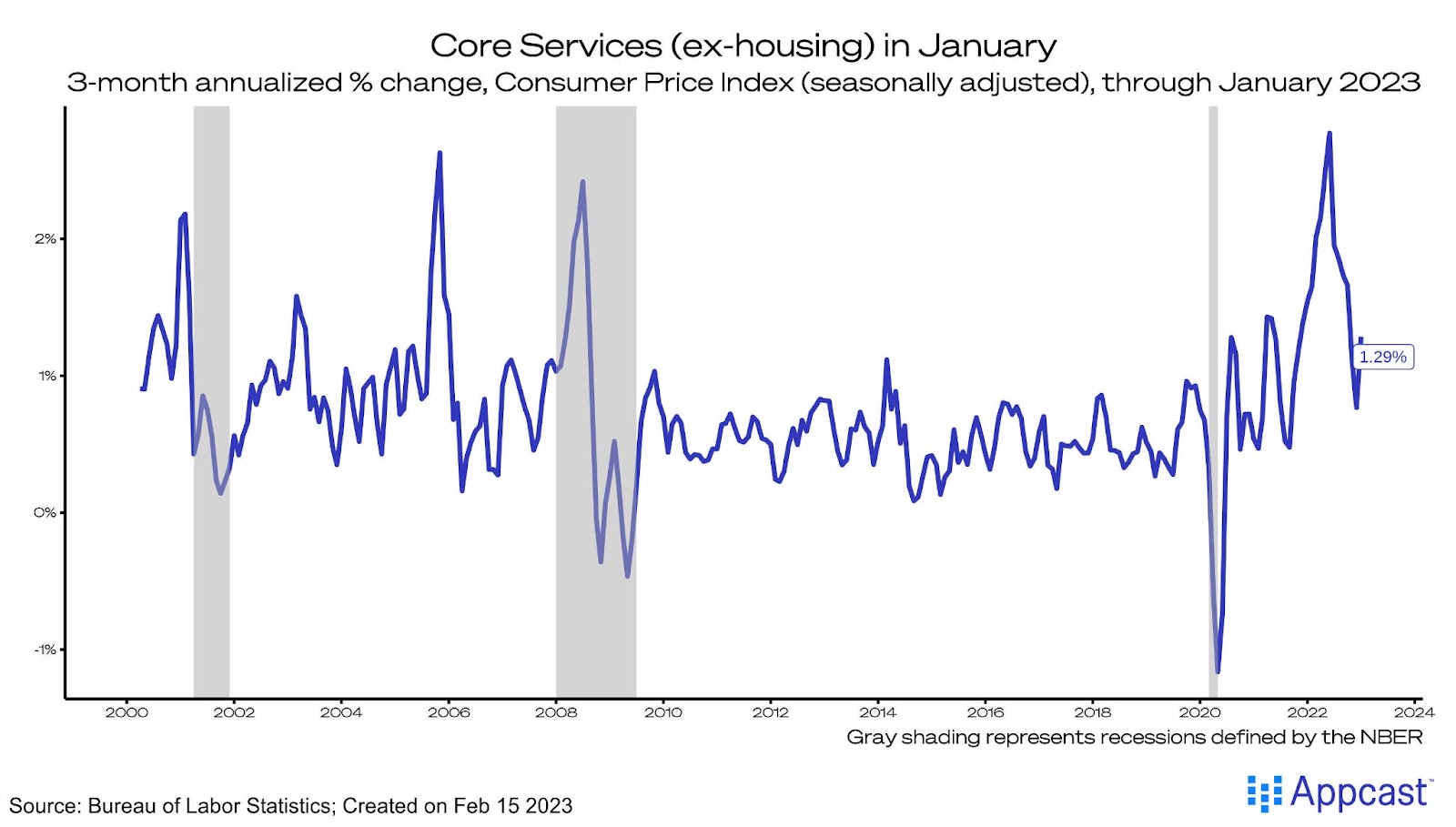

But even supercore inflation, which is the core of the inflationary onion that the Fed has decided to focus on, is proving to be sticky. Stripped from housing, this category of inflation has become central to the narrative in part because of how tightly the category is tied to the labor market and impacted by shifts in labor costs. Unfortunately, it rose slightly in January, suggesting that inflation cannot simply slip away. The Federal Reserve’s focus on cooling the labor market will have to continue; inflation may remain uncomfortably hot for as long as the labor market runs seriously hot.

The good news is inflation is still moderating, but the pace of that moderation is slowing. Disinflation may not be as “immaculate” as we previously believed. In this era of inflation, reading too much into a single month of data can be deceiving and misleading. Instead, focus on the emerging trends, which in this case is slow moderation. Inflation will be with us for some time, no matter what lens you decide to look through.