Disinflation is happening, but slowly.

In March, headline inflation slowed to 5% from the year before, the slowest pace in over two years. Price growth is moving sideways. This is a good thing in the eyes of markets, as the risk of stagflation – stubbornly high inflation paired with stagnant economic growth – is declining. This is a positive in the Fed’s eyes as well, but it would like to see a faster return to its 2% target, especially in the stubborn services sector.

Breaking it down

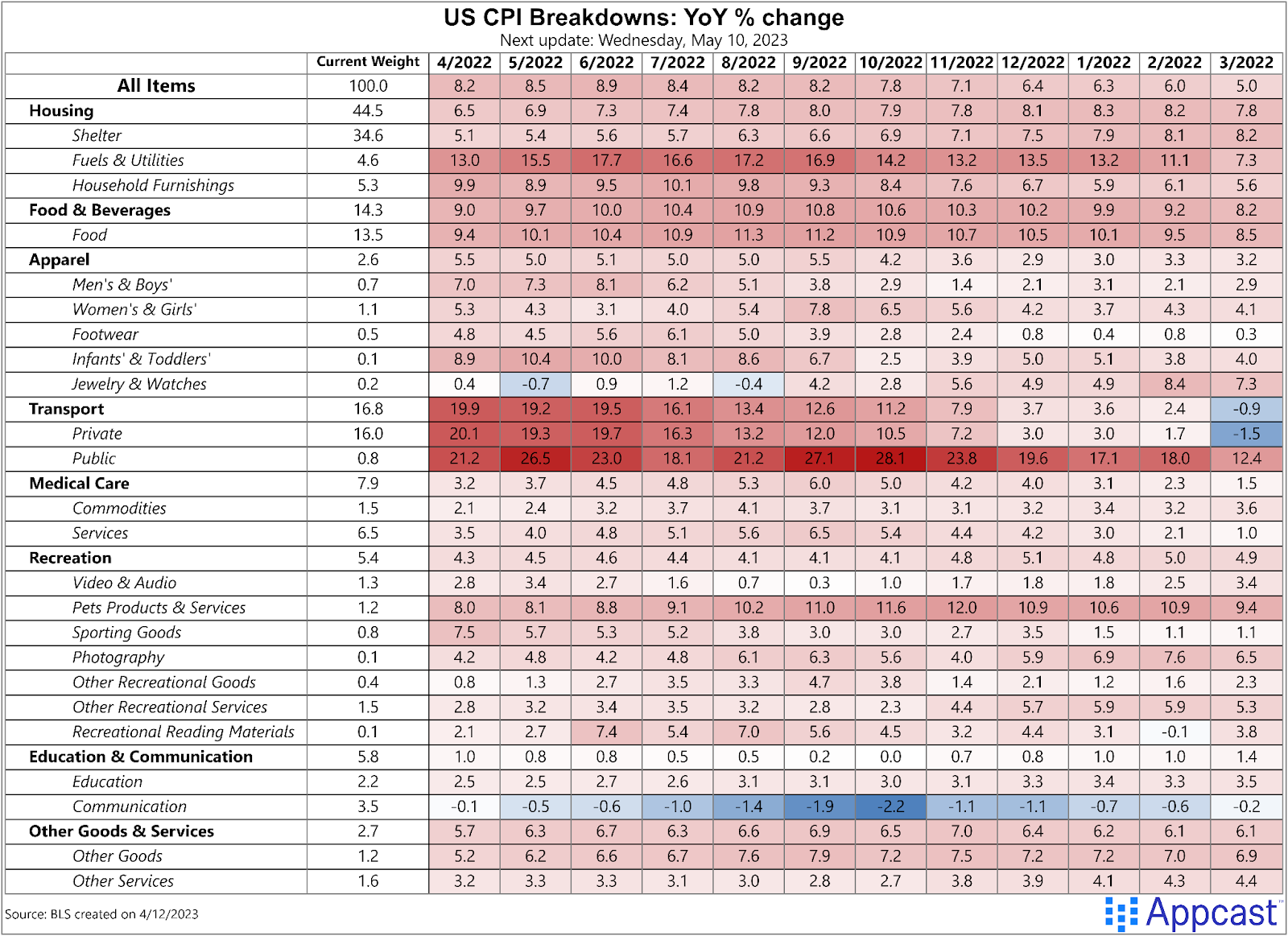

In the three months through March, the Consumer Price Index (CPI) rose at a 3.8% annual rate, a slight deceleration. Huge declines in energy prices contributed to this slower pace of increases, but high prices for food continue to plague U.S. households.

“Core” CPI (excluding volatile food and energy prices) was flat at 5.1% (annual rate) in the same three-month period. Despite the shakeup in credit markets in March and the Fed’s continued tightening cycle, these core prices have yet to budge. Too-high prices continue to pinch Americans’ pockets – a reminder that though the fight for price stability is going in the right direction, it is far from over.

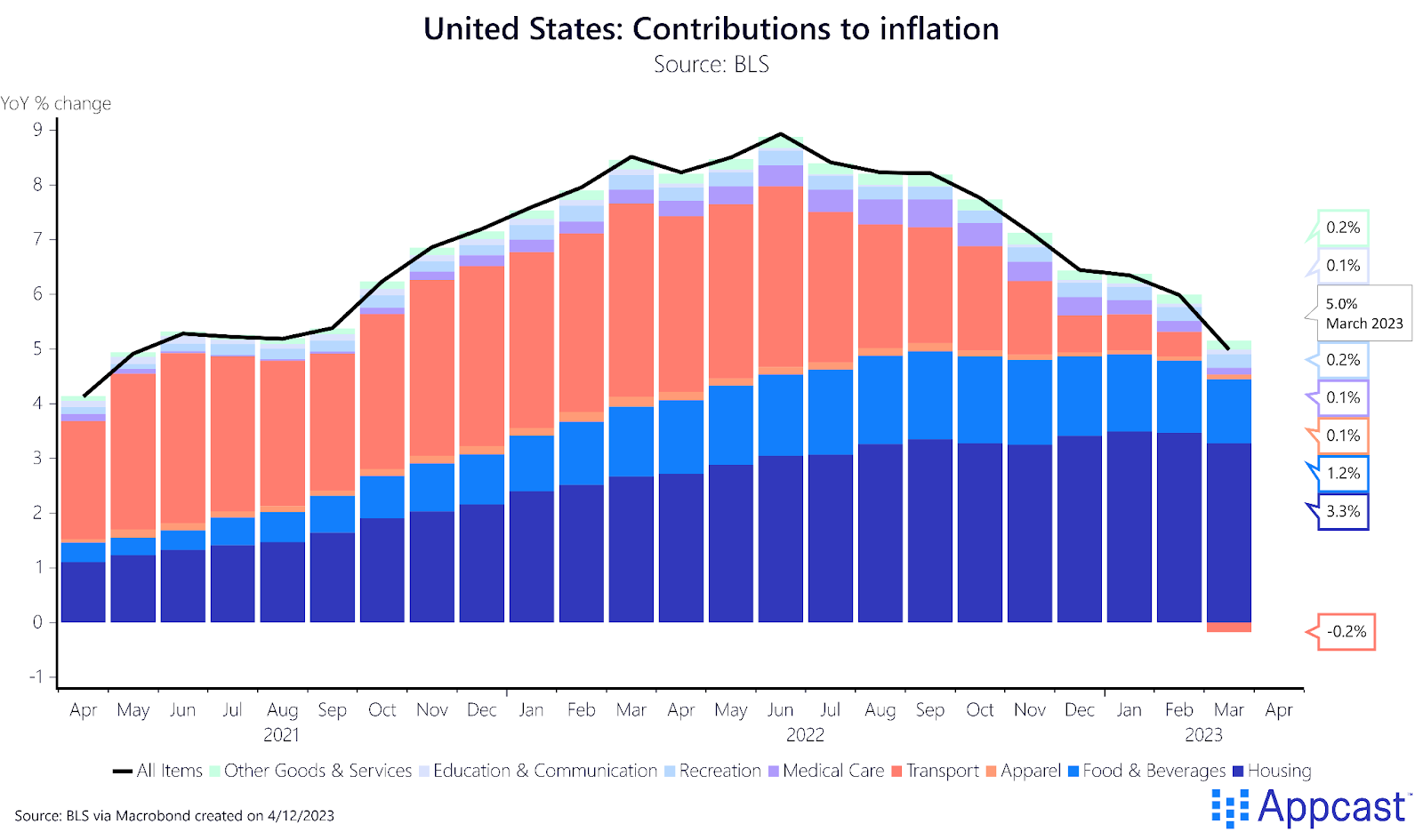

Housing is especially persistent and continues to be, by far, the biggest contributor to inflation.

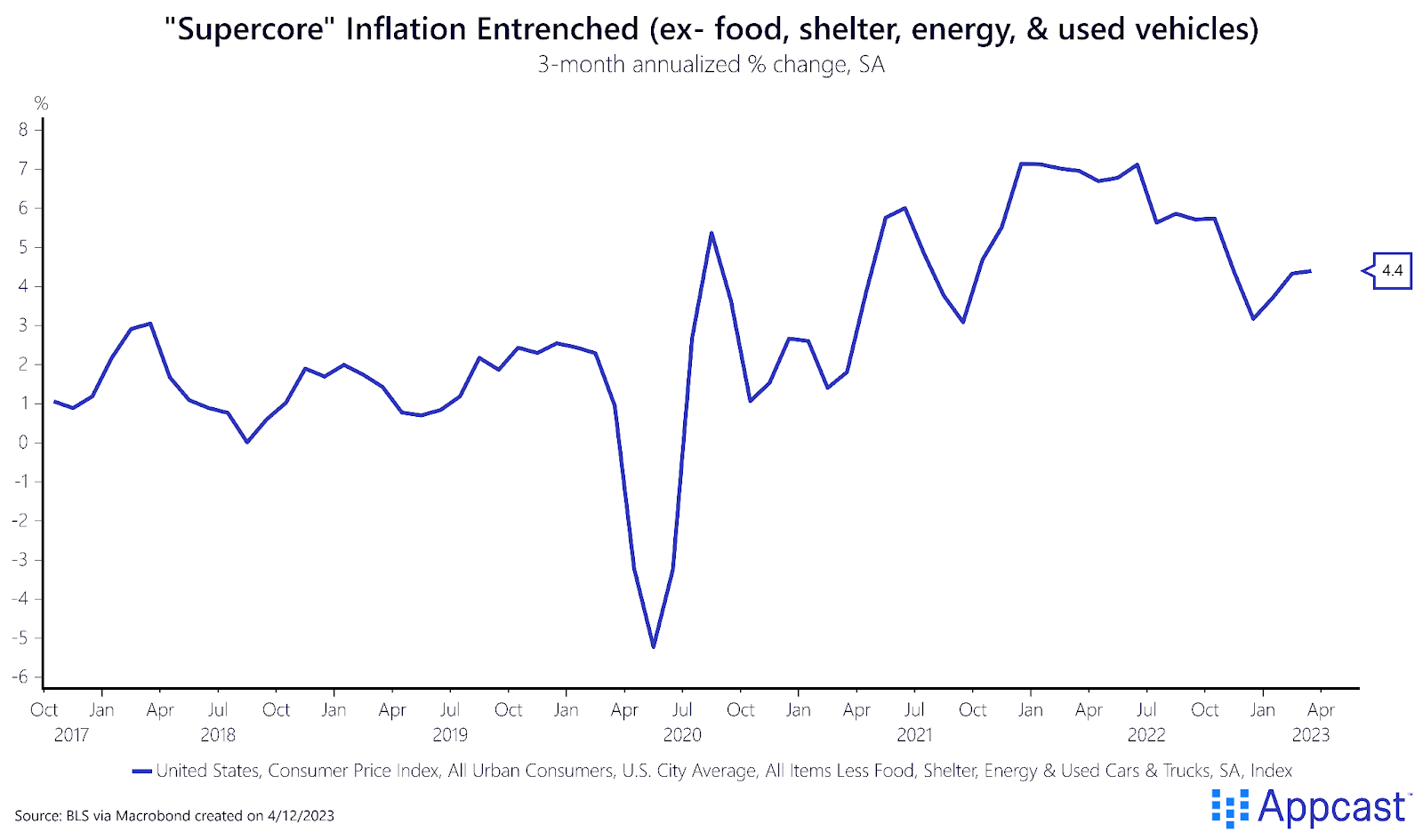

“Supercore” inflation, which strips out housing and vehicles and other volatile components, moved sideways in the three months through March. This measure focuses on services inflation, which has been the Fed’s focus after goods and energy prices began to subside. It is here where the tight, but slightly softening, labor market makes its mark. Strong wage growth and high demand has contributed to the stubbornly high, nearly entrenched, prices in services. These prices, like housing inflation, tend to be stickier – once they rise, they’re harder to bring down.

Hot or not: a shift in pressures

As mentioned above, housing continues to be the largest contributor to inflation. However, other price pressures are subsiding. Americans are seeing cheaper prices for transportation, and seeing smaller increases on necessities like education and recreation. The two charts below show how the nature of price increases has changed during this inflationary period, which underscores the continued pressure on the Fed. All in all, this report was neutral to slightly positive: the cooling in headline inflation is a comfort, but the stubborn prices in services signal upcoming problems for the Fed.