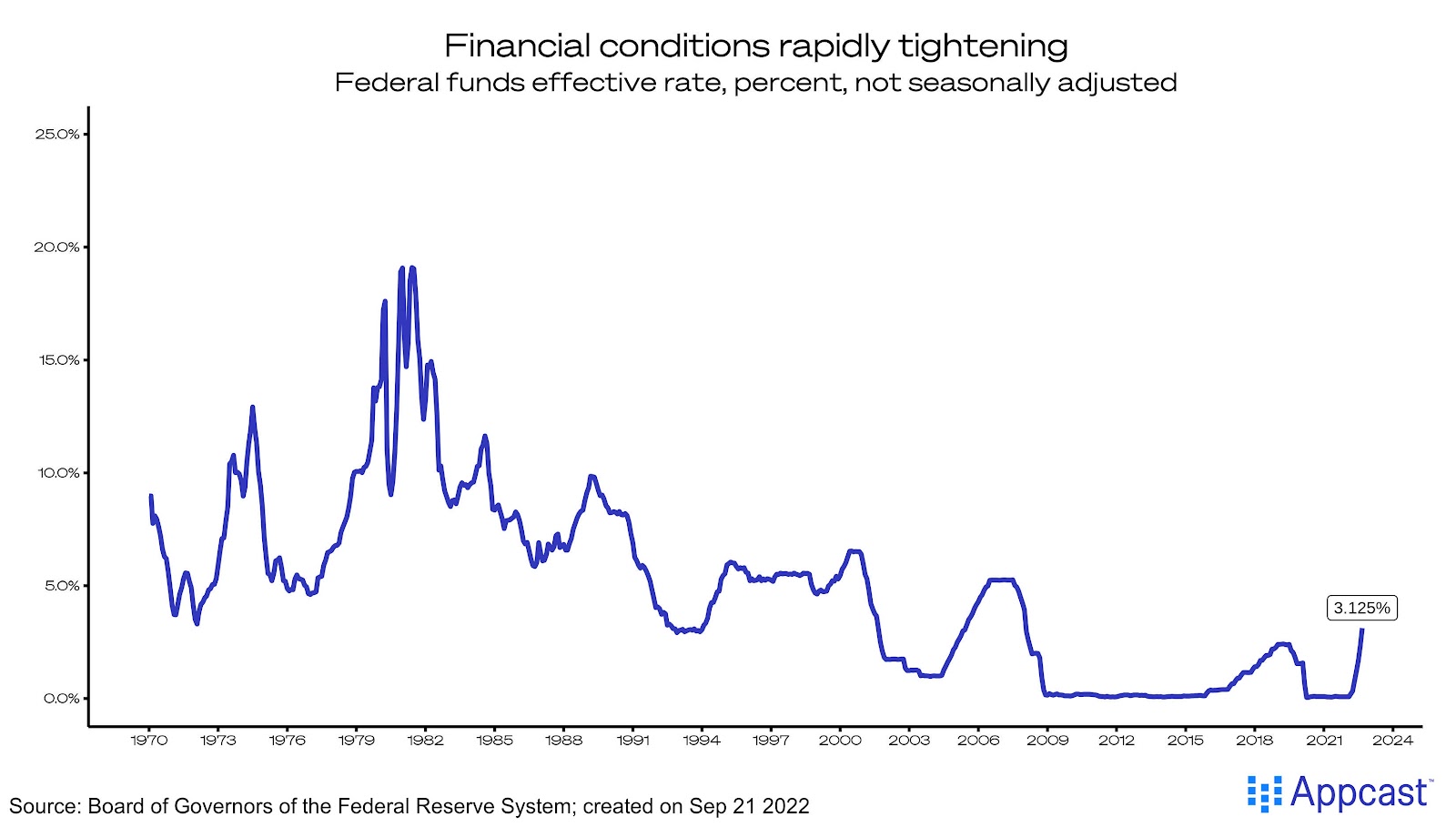

The Federal Reserve raised its benchmark short-term interest rate by 0.75 percentage points, the third consecutive such increase. Fed Chair Jerome Powell signaled that this would not be the end; increases will continue until the inflation rate is safely in reach of the 2% target.

Since June, hope for a soft landing has substantially eroded among Fed officials. New projections by Federal Reserve Board members and Bank presidents indicate more pain may be in store for the labor market. To return to a healthy level of inflation (the Fed’s 2.0% inflation target) by 2025, unemployment may need to rise as high as 4.4% in 2023, up from a 3.9% projection in June.

How high the unemployment rate must rise to tackle inflation has been a roaring debate this summer. It seems the Fed has accepted that decreasing labor demand – in the form of fewer job openings – may not be enough.

Additionally, GDP growth projections were significantly declined: in June, the Fed projected growth of 1.7% in 2022. Today, just three months later, this projection has fallen to 0.2%. For 2023 and 2024, growth projections were also shifted lower.

The Fed is signaling that the U.S. economy will not emerge unscathed from this inflationary environment. But, as Powell was clear to state, sacrifices today to bring inflation down will decrease the chance of long-term economic devastation.