Inflation is turning a corner. Growth is slowing but still positive. The labor market is resiliently strong. Simply put, it seems that the U.S. economy is undergoing an “immaculate disinflation” – whereby price growth slows to normal but without collateral damage to the labor market. But it’s too soon to rule out a hard landing – aka, recession.

Soft-landing optimists were cheered on by the Consumer Price Index (CPI) report for December 2022, which showed monthly deflation (a decline in the overall index). The month-over-month decline was primarily because of falling energy prices. Price growth over the previous year decelerated to 6.4% (the orange line in the chart below). “Core” inflation (which strips out notoriously volatile food and energy prices) rose by 5.7% over the previous 12 months.

This is a notable improvement. But is falling inflation, dare I say, transitory? The Fed must be happy with this third consecutive “good” CPI print, and in likelihood interest rate hikes will become more gradual. The future of the labor market in 2023 – for both job seekers and recruiters alike – hinges on the future path of inflation and how the Fed responds to it.

Put aside energy, food, and commodity prices, which are largely beyond the Fed’s control. As for what is left – “core” inflation – let’s break it into three parts in accordance with Fed Chair Jay Powell’s recent speech: core goods, housing, and core services (ex-housing).

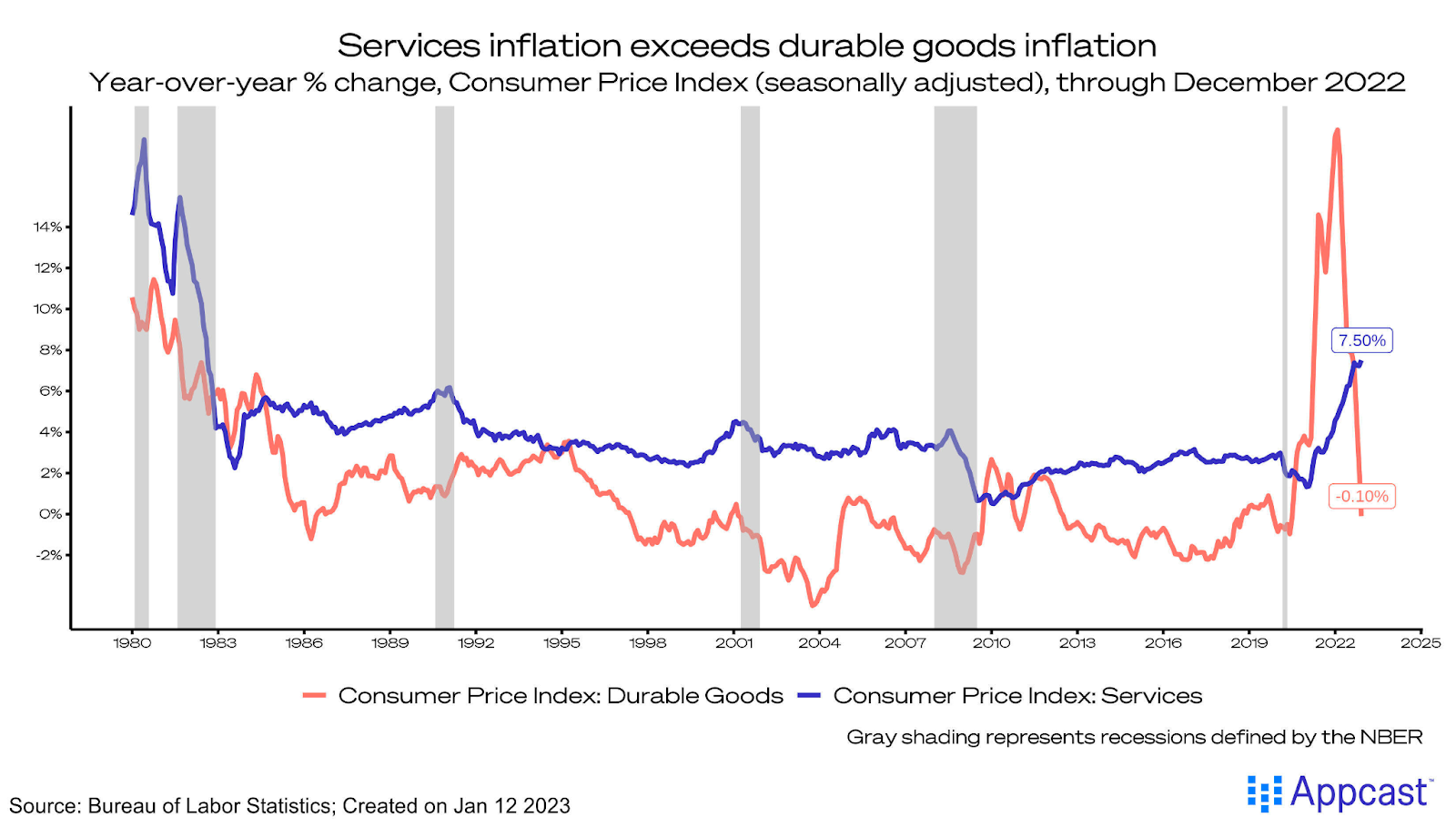

Core goods deflation is well underway now that supply chain bottlenecks have largely been cleared. The chart below shows a sharp plunge in prices for durable goods, which are actually negative year-over-year.

Housing is unique. The CPI’s notion of housing inflation – “owner’s equivalent rent” – has been rising very strongly, but seeing as how real-time rent growth (in the form of new leases) has gone negative, it’s only a matter of time before housing costs “roll over” in the CPI calculations, lowering inflation further.

That brings us to the third and most important category: core services (ex-housing) inflation. This is critical for the labor market as the Fed believes services prices are largely driven by labor costs. Thankfully, in recent months, wage growth has moderated. The Fed, if not trying to engineer a recession, is willing to accept higher unemployment to bring down wage growth and, by extension, core services inflation.

Core services (ex-housing) prices have flattened, with a 3-month annualized rate of change just above zero. This is the “disinflation” part of the “immaculate disinflation” bit. Simply put, prices for core goods are falling because supply chain stress has lessened and demand has cooled; prices for core services are cooling due to a mix of factors, but principally from moderating wage growth.

So far, though, this disinflation isn’t leading to widespread layoffs – the “immaculate” part. Despite higher interest rates, the labor market remains extremely “tight,” with 1.7 job openings for every unemployed job seeker and the unemployment rate at a 50-year low. Tech layoffs, which are, of course, devastating for those workers, have yet to spread to the broader economy.

Even as recent inflation readings have been encouraging, a “hard-landing” (recession) remains a distinct possibility. Two risks in particular come to mind: (1) a surge of COVID cases in China leads to global supply chain disruptions and (2) Russian aggression in Ukraine goes to a new level, triggering another “supply shock” to global energy prices and/or risk appetite among investors. As of today, economic growth is slowing, but that is by the Fed’s rate-hiking design. In 2023, the unemployment rate is most likely to increase, but even the Fed’s projected 5% unemployment rate is consistent with a solid economy.

If the goal of a “soft landing” is cooling inflation without a material rise in layoffs, that is what the hard data is showing. It may take a few months, but core inflation should come down sufficiently to give the Fed room to pause rate hikes. If the labor market continues to hold up with this strength, we may very well get immaculate disinflation. I see an economy that could weather 2023 with more strength than many recession-doomsayers envision.