Some months ago, I discussed how rising interest rates would impact the labor market and specifically which industries the tightening cycle could upend. The two most at risk? Construction and manufacturing. Almost a year and 375 basis points later, these two sectors have not only survived this tightening cycle – they have thrived. Sure, the housing sector had a worrisome wobble, but the construction sector has been propped up by increased investment in manufacturing projects. A weaker housing market and a decrease in the demand for durable goods couldn’t compete with the deluge of investment – much of it spurred on by the federal government – that strengthened these sectors through a period of economic headwinds.

A Helping Hand

How has manufacturing managed to defy the slowing expectations? The sector found a helping hand in the (perhaps too-appropriately named) CHIPS Act passed in 2022.

The CHIPS act explicitly targets the manufacturing sector, specifically the manufacturing of semiconductors. Spooked by pandemic-related supply chain snarls, the current administration initiated new investment aimed at reshoring manufacturing of these chips – today, the U.S. produces just 12% of semiconductor chips, compared to over 30% in the 1990s. Mending that gap is no easy task, but $280 billion is sure to help. Of that absolutely-bonkers figure, over $50 billion is directly aimed at semiconductor manufacturing, including new employees and workforce development.

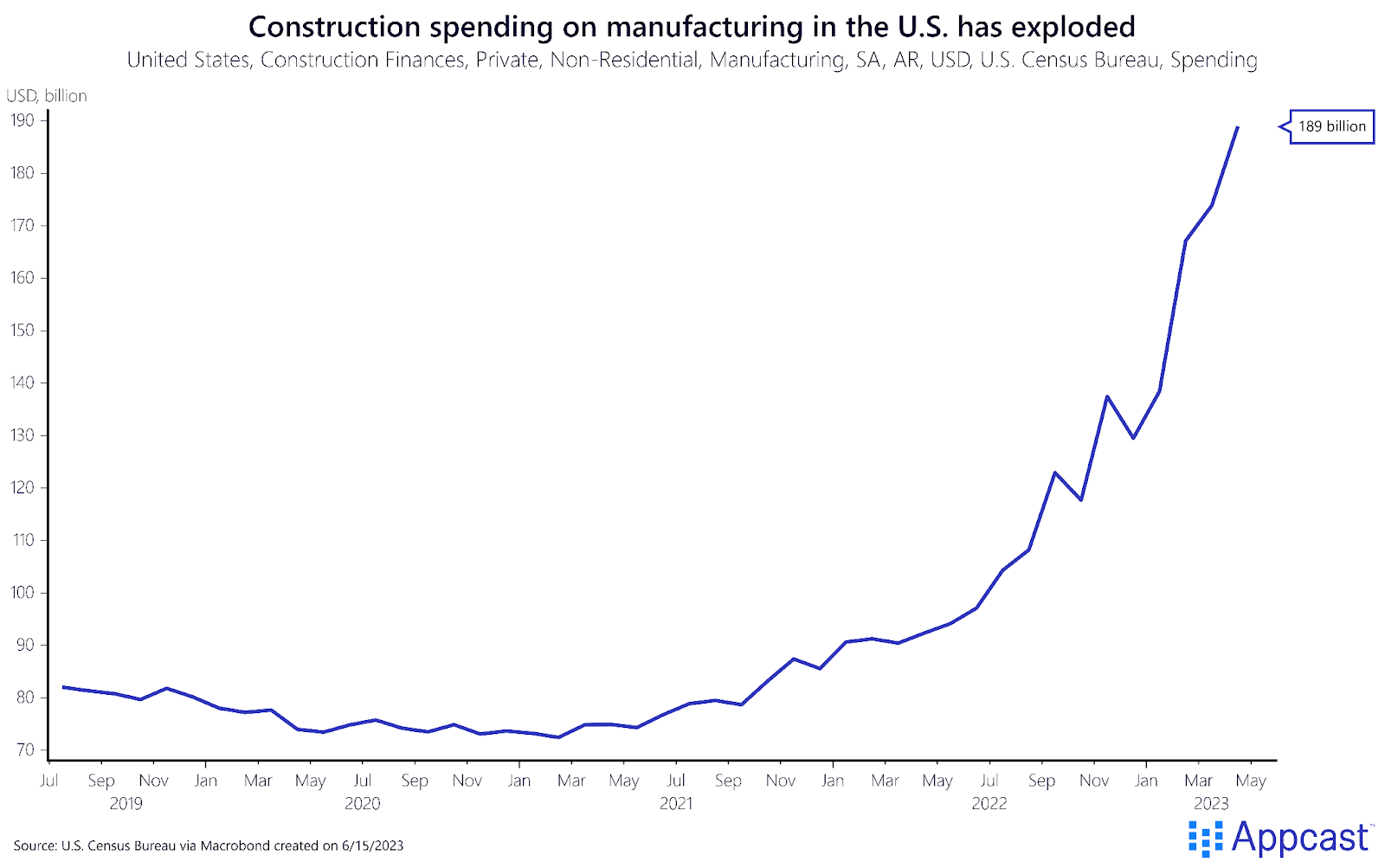

This infusion of investment has carried the construction sector through a difficult period. While housing, offices, and healthcare construction spending has steadied, manufacturing construction projects have boomed, with spending up 104.6% in April from the year before!

Manufacturing construction spending as a share of GDP is also impressive, increasing to a 0.7% share after a post-COVID dip. The largest projects contributing to this increase are related to semiconductor production, as well as sustainability initiatives connected to the Inflation Reduction Act.

Labor market outcomes

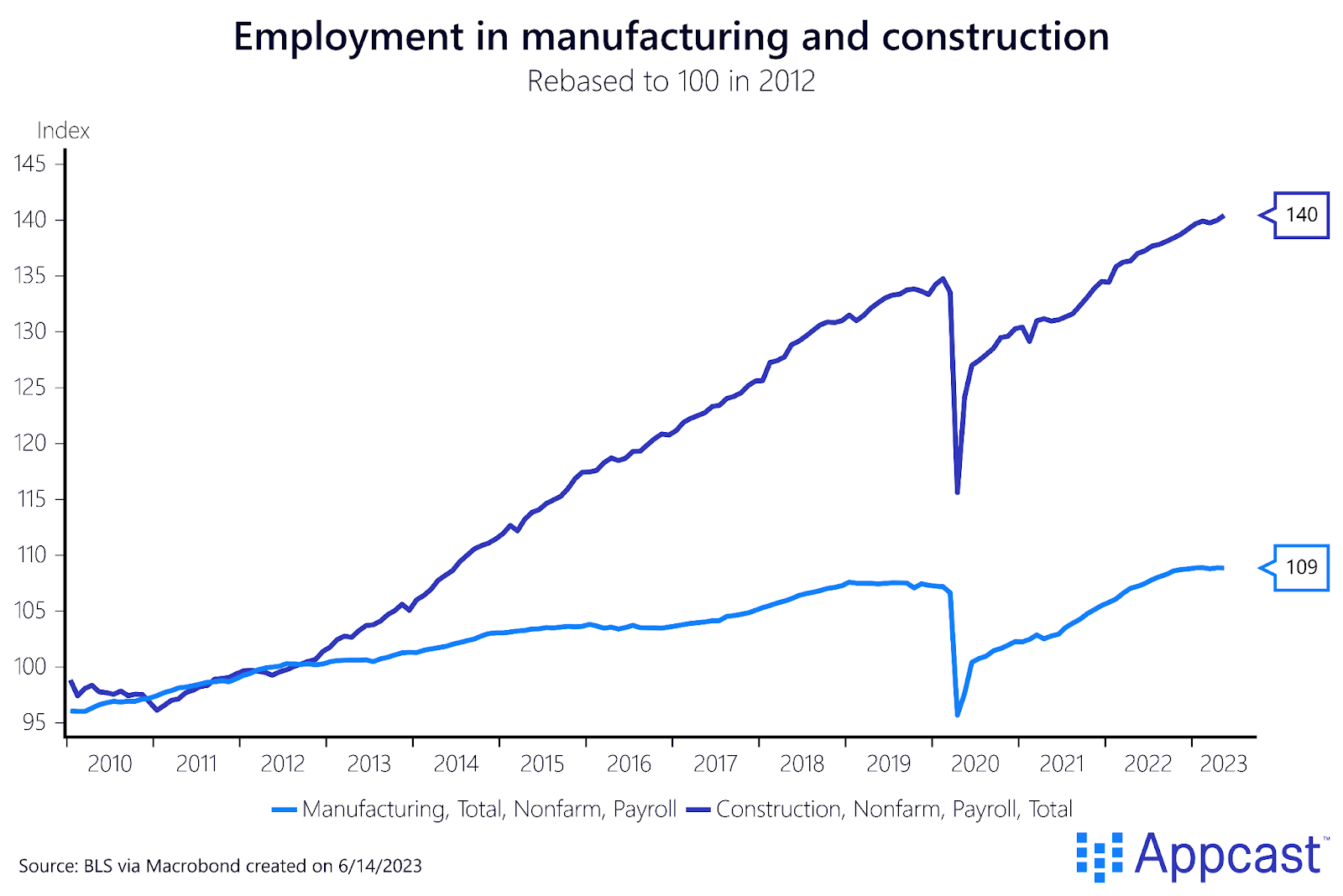

As this investment and reshoring initiatives make their way through the construction and manufacturing industries, it has been beneficial for employment in those sectors. Construction payrolls have skyrocketed since the set back during the pandemic and the growth shows no signs of slowing.

In manufacturing, growth has been more subdued but the demand for growth is there. Openings in the sector have fallen slightly in recent months but remain 71.6% above February 2020 levels. Manufacturers have taken the reshoring initiatives to heart, urgently recruiting new workers, but the pace of employment growth has struggled to keep up.

The manufacturing and construction sectors have avoided a downturn that the Federal Reserve’s tightening cycle threatened to create. An infusion of new money has elevated demand for labor and buoyed new projects. And, on top of this investment wave, many global manufacturing companies with a presence in the U.S. have made a commitment to “reshoring” facilities, having been scarred by the supply chain snarls caused by the pandemic.